It’s been a brutal stretch for crypto, tech stocks, and growth more broadly. The Nasdaq-100 just posted its worst three-day rout since April’s Liberation Day meltdown and Bitcoin has been cut in half from its October highs, briefly touching $60k on Thursday before finding temporary footing. Over $2.7B in crypto positions were liquidated in a 24-hour window, with 85% of those being longs.

X is convinced, perhaps rightfully, that this is the “worst crypto winter ever.” While we are nowhere near the largest drawdown in percentage terms, what has made this stretch feel so painful is that the selloff is isolated to our corner of the market.

Pick a fintech stock or crypto token out of a hat and it’s likely down 40-70% from ATHs just last year. But for the broader market it’s been just fine. The S&P 500 is only a few percent off its all-time highs. The Dow Jones Industrial Average, containing 30 sleepy “blue-chip” companies that have been around for decades, just crossed 50,000 for the first time in history.

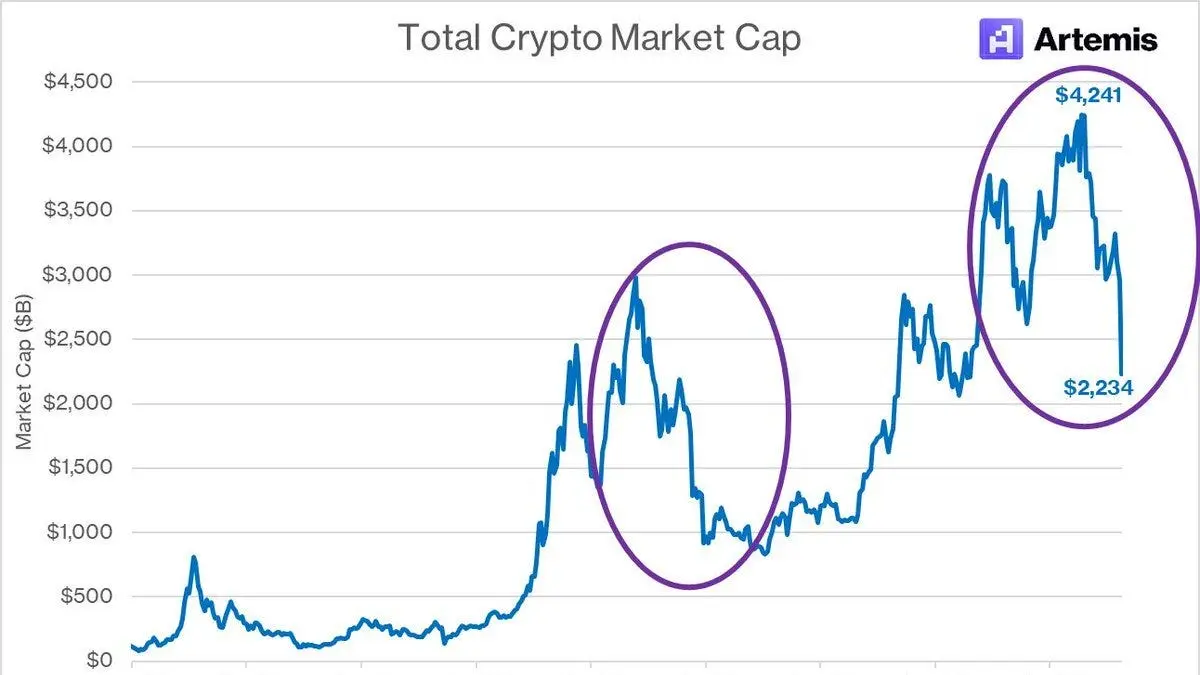

Main Street, allocated to index funds and fixed income, is chilling while growth chasers still accumulating for retirement (aka Millennials and Gen Z) are suffering. The crypto winter in 2022 sucked but everything was down; Meta had a larger peak to trough (-77%) than broader crypto (-75%). Cutting rates as inflation retreated was the tide that rose all ships. Now, crypto is staring at a -50% drawdown and record $2 trillion wiped off its market cap while inflation is low and the FOMC has cut rates 7 times.

The selloff has also been remarkably fast. The last 3 weeks have seen 3 consecutive -$10k candles from Bitcoin as we’ve fallen from $96k to the $60k range. Again, this pattern looks strikingly similar to 4Q21 - 1H22, where we had a one-two punch to the gut that roiled markets. But inflation isn’t heading to 9.1%, corporate profits aren’t getting hit, and the Fed isn’t embarking on its fastest hiking campaign since the Volcker era of the ‘80s.

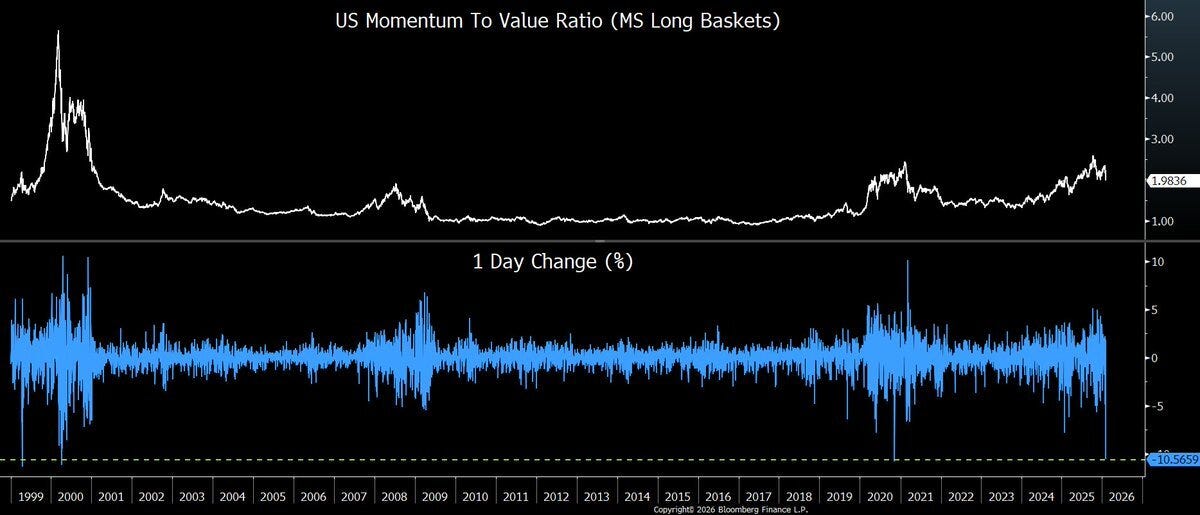

All this begs the question - what the hell is going on? In a word: rotation. After three consecutive years of double-digit returns powered by a historically narrow set of AI and momentum names, the regime is changing. And in true market fashion, we have overshot the momentum downside as value has finally caught a bid after years of underperformance.

Wednesday gave us the most visceral illustration of this dynamic. The iShares MSCI USA Momentum Factor ETF (MTUM) dropped 3.7% - its worst day since Liberation Day - a day BofA’s trading desk claims is the second-worst single-day drawdown of the last decade.

Goldman’s desk said there was “no smoking gun” for the move, chalking it up to short-term performance technicals getting too extreme after years of one-directional crowding. That’s probably right. When everyone owns the same winners and the same losers, the unwind can be savage even without a fundamental catalyst. And the winners had gotten very crowded. The top 10 stocks in the S&P 500 had ballooned to nearly 40% of index weight, the most concentrated the market has ever been.

The broader story here is one of generational portfolio pain. If you’re 55, allocated 60/40 to index funds and bonds, this drawdown barely registers. If you’re 30, overweight tech, fintech, and crypto because that’s what’s worked your entire investing career, you’re staring at a 40-60% drawdown in the stuff that matters most to your net worth, while the financial media is telling you the market is “only a few percent off highs.”

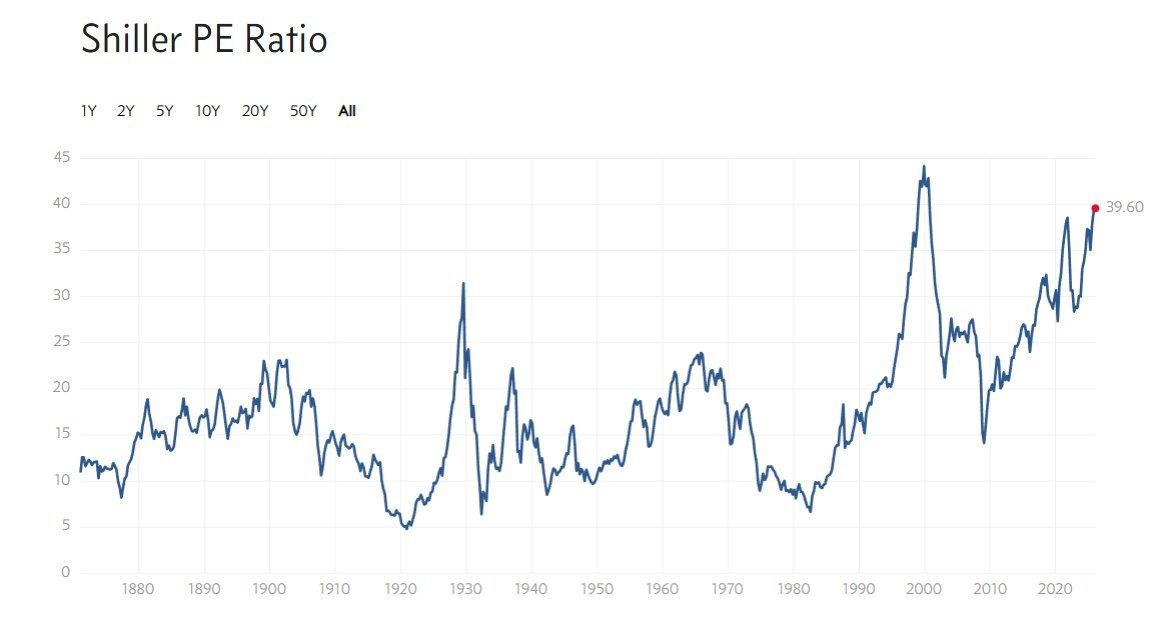

The CAPE ratio (cyclically adjusted P/E) hit 40 coming into this year, a level only seen at the peaks of 1929 and 2000. Something had to give, and what gave was the most speculative, most momentum-driven, most crowded corner of the market. Our corner.

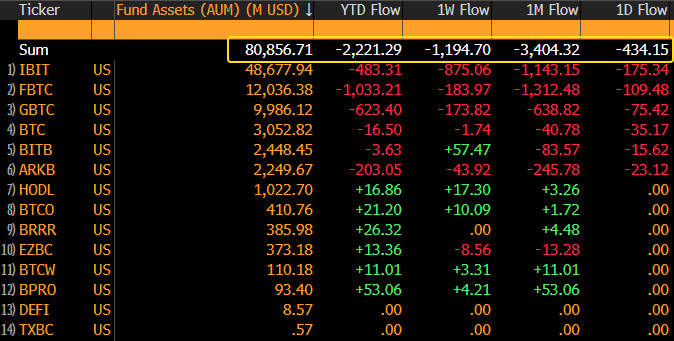

The silver lining for this crisis is institutional flow. For Bitcoin, ETFs comprise ~$103B of AUM, or >7% of Bitcoin’s market cap. Every month since October has seen outflows, but cumulatively they only amount to a high-single digit percentage of Bitcoin’s market cap. In other words, ETFs’ drawdown from $165B to $103B AUM has been driven “inorganically” by the underlying, and there is no reason to believe the ecosystem is permanently impaired from a flows perspective.

The first spot Bitcoin ETFs launched in January 2024 and were not there as sources of demand during previous bear markets. This could be a double edged sword though, as these ETFs are now dumping incremental supply onto fragile markets. Only time will tell whether they exacerbate or mitigate crypto drawdowns in the short-term, but in the medium to longer term it’s hard to argue their existence is a negative.

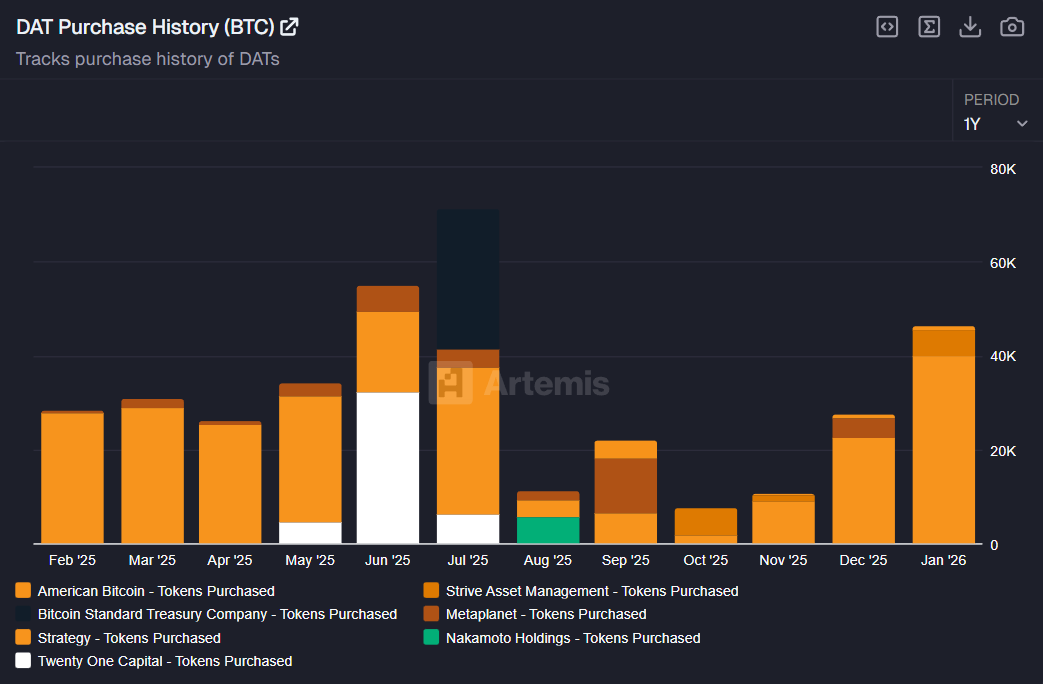

DATs are a different story. All DATs (not just Bitcoin) are underwater, with their cost basis exceeding the current spot price for Bitcoin. DATs currently hold ~$53B (or ~4%) of Bitcoin market cap, though flows since their PIPEs are almost entirely retail driven, versus ETFs which are historically more split with institutions. Just look at the largest 13-F holders of Bitcoin - they’re almost all using IBIT 4.26%↑ as their vehicle of choice rather than a DAT.

However, Strategy remains an incremental purchaser of Bitcoin as the world’s first and largest DAT. Strive has also been buying Bitcoin, albeit on a smaller scale. Going forward, given mNAV has compressed to ~1x or lower for most DATs, and preferred stock such as STRC 2.04%↑ and SATA 5.63%↑ remain well below par making ATM issuance impractical, the magnitude of secondary offerings in the future should be much smaller.

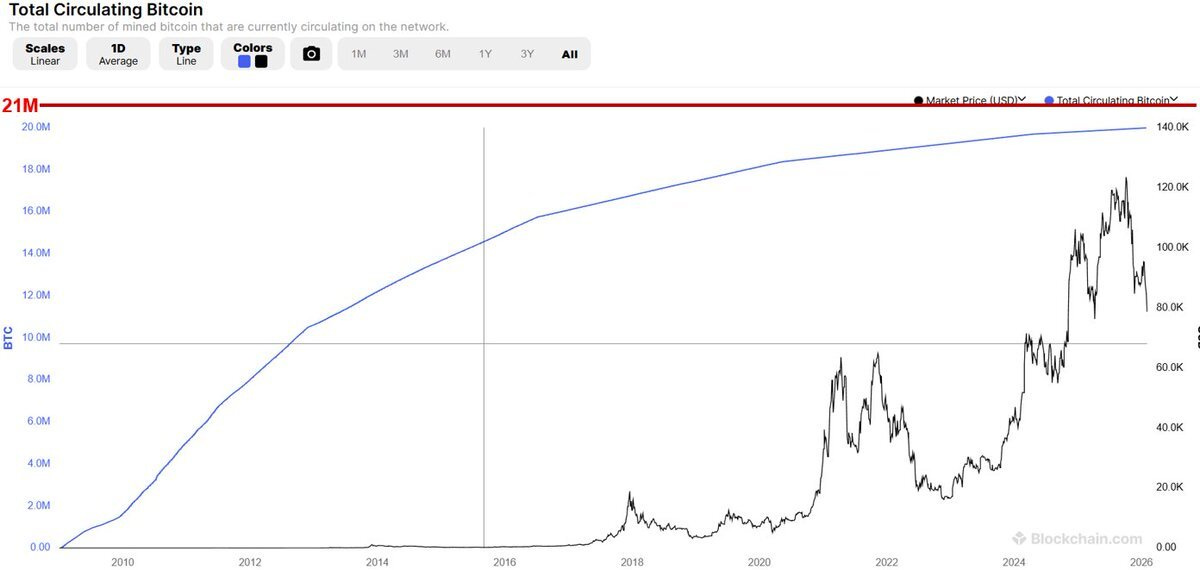

What is the floor for crypto? Well, history has shown that Bitcoin usually troughs right below mining costs, and can hang there for a while before retracing higher. The reason for this is simple - once all-in costs exceed spot Bitcoin prices, it doesn’t make any sense for miners to continue powering costly rigs to mine more Bitcoin. Turning off the taps thus leads to slower supply growth, and becomes an Econ 101 supply and demand story.

Estimates are all over the place for mining costs in Q1 2026, but I’ve seen anywhere from ~$60k for the lowest cost miners (like TeraWulf) on high-end S21 Pros with easy and cheap access to power, to ~$90k for those using legacy rigs with less favorable energy costs.

So is the floor for Bitcoin $60k? Is that why we got such a hard bounce the moment we hit $60k last night? Well, not quite. For one, the 2018-2019 bear showed us that Bitcoin can spend up to 6 months and 20% below mining costs. And past performance is not indicative of future results - we just don’t have enough history to make such a bold claim.

Furthermore, in the 2018 bear market about 16 million Bitcoin was circulating out of 21 million that can ever be mined. This gap of 5 million was meaningful, representing 25% of total supply that would hit the market at a slower pace as miners powered off. Today, we sit just under 20 million circulating Bitcoin. An incremental 5% isn’t really enough to make a supply difference, when there are so many other dynamics at play.

In short, crypto price action is now a story of demand rather than supply, and for the former institutions are on our side.

As for stocks, the market has been driven by narrative rather than empirical evidence. Money has flowed out of intangible software, which can be displaced by AI, into producers of physical goods - the hard economy. Of course this is overblown.

When you see a stalwart software compounder like Constellation $CSU drawn down 50%, you know insanity is afoot. These stocks haven’t even reported Q1 earnings yet but have faced their fastest declines ever YTD. The patient will be rewarded, and time arbitrage has never been higher.

So where does that leave us? The temptation in moments like these is to reach for historical analogs and declare either “this is 2022 all over again” or “this is just a healthy correction.” The honest answer is it’s neither. The macro backdrop is fundamentally different from 2022.

The good news is that the structural tailwinds for crypto and fintech haven’t disappeared. ETF infrastructure is intact and institutions haven’t fled, they’ve just stopped adding. Regulatory transparency via the Clarity Act has been delayed but not axed, and a more constructive SEC posture is real.

The hardest part of this whole ordeal has been the mark-to-market losses in our portfolios while the rest of the market barely flinches. That is new and uncomfortable for a generation of investors who have never known a world where crypto goes down while the Dow goes up. However, time is on our side, and this is the environment where actual long-term returns are made.