Hey Fundamental Investors,

Jon here again from Artemis.

We’ve deep-dived: Strategy, CoreWeave, Coinbase and Circle.

Today, we take a deep-dive into Hyperliquid, a leading decentralized perpetuals exchange. I think of Hyperliquid as more of an onchain fintech app that dominates onchain exchange volumes and is pulling in traditional fintech / stock investors as a strong fundamental play.

As always, this is not financial advice—just a framework for thinking through potential upside and risk, using data and valuation modeling for Hyperliquid based on comps.

Let’s dive into Hyperliquid with our fundamental analyst, Kevin Li.

Executive Summary:

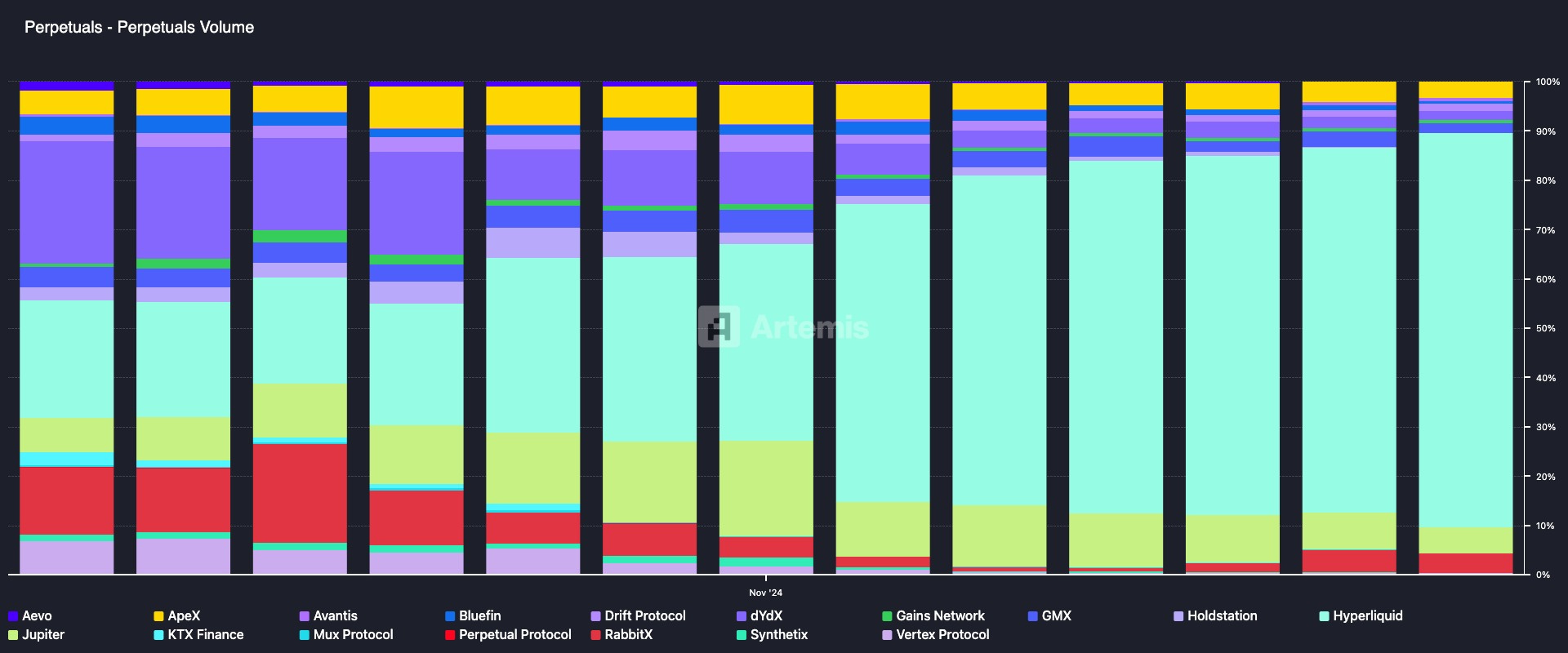

- Market Dominance in Decentralized Perpetuals: Hyperliquid commands over 75% market share in decentralized perpetuals by delivering CEX-level speed and UX on a custom Layer 1 with a fully on-chain Central Limit Order Book (CLOB).

- Significant Potential in Spot Trading: Currently, Hyperliquid is uniquely positioned to capture a substantial share of decentralized spot trading, leveraging its performant on-chain CLOBs and the Hyper Unit protocol for secure cross-chain asset bridging.

- Expanding Ecosystem as a DeFi Infrastructure Layer: Hyperliquid is evolving into a full DeFi infrastructure layer with HyperEVM, attracting foundational apps in lending, staking, and stablecoins, and surpassing $1B in TVL.

- Permissionless Innovation for Future Growth: Hyperliquid Improvement Proposals (HIPs) are foundational upgrades shaping the future of decentralized finance. HIP-1, HIP-2, and HIP-3 establish a fully permissionless, scalable trading ecosystem—powering community-led listings, trustless liquidity, and unrestricted market creation across both crypto and traditional assets.

- Robust Value Accrual and Tokenomics: Hyperliquid's native HYPE token benefits from a highly aggressive buyback model, returning 97% of trading fees to token holders, and features a fixed 1 billion supply with a community-first distribution that fosters strong alignment.

- Undervalued by Traditional Metrics: Despite strong growth and fundamentals, a sum-of-the-parts analysis—using Robinhood and Coinbase as comps—suggests Hyperliquid is undervalued, with a fair value range of ~$51.05–$59.62.

- Market Expansion, Not Direct Competition: While Coinbase and Robinhood are entering the perps market, they currently offer lower leverage (5x and 3x, respectively) and have yet to demonstrate the ability to bootstrap liquidity effectively. As a result, Coinbase and Robinhood appear to be market expanders rather than direct competitors to platforms like Hyperliquid.

Hyperliquid: The Rising Star in This Crypto Cycle

As one of the best performing token, Hyperliquid is a decentralized exchange (DEX) that has gained rapid traction by replicating the speed, liquidity, and user experience of top centralized exchanges (CEXs) like Binance. In doing so, it has captured over 75% market share in the perpetuals (perps) segment, outperforming rivals on both product quality and protocol economics. Since its Token Generation Event (TGE), HYPE has surged 4×, fueled by real user adoption, strong fee generation, and one of crypto’s most aggressive buyback models—returning 97% of trading fees to token holders.

The core thesis is this: Hyperliquid isn’t just a high-performing DEX—it’s a foundational layer of DeFi infrastructure. With CEX-level performance, a platform-style roadmap, and a tightly aligned token model, it’s designed to lead the decentralized derivatives market and more. Traditional valuation frameworks fail to fully capture the scale of what Hyperliquid is building—or the growth potential that still lies ahead.

The Market Shift: Spot Thrives, Derivatives Lag—Until Now

To understand Hyperliquid’s success, we first need to examine the state of decentralized exchanges. This cycle has seen a notable surge in decentralized spot trading: once a niche corner of the market, DEX spot volumes now represent over 20% of CEX activity. In contrast, decentralized derivatives have lagged behind—until recently. Signs of momentum began to emerge in late 2024, largely driven by Hyperliquid’s rise. Yet the adoption gap between spot and derivatives remains wide, highlighting persistent frictions in decentralized perps infrastructure.

To understand why this matters, it’s worth zooming out for a moment. In crypto markets, spot trading refers to the immediate exchange of assets—similar to buying stocks outright. Perpetual futures (or perps), on the other hand, are derivative contracts that let traders speculate on price movements without owning the underlying asset. Unlike traditional futures, perps don’t expire, making them ideal for continuous, leveraged trading. Importantly, on centralized exchanges, perp volume routinely exceeds spot by several multiples. For sophisticated traders, hedge funds, and institutions, perps are the primary tool for both speculation and hedging.

The recent rise in DEX spot adoption can largely be attributed to the explosion of long-tail asset trading within the Solana ecosystem. Platforms like Pump.fun, Raydium, and Jupiter have created a vibrant environment for small, community-driven tokens. According to Blockworks, meme coin trading now accounts for a substantial portion of total spot volume. But while retail engagement is growing, blue-chip asset trading on DEXs remains limited.

Why Decentralized Trading Lags Behind

To understand the limited adoption of decentralized perpetuals and blue-chip spot trading, it's important to compare the two core DEX liquidity architectures—Automated Market Makers (AMMs) and order books—and examine how each has shaped the development of spot and derivatives markets.

Order books, the golden standard in traditional finance and centralized crypto exchanges, provide deep liquidity, accurate pricing, and advanced trading features like limit orders and high-frequency execution—capabilities crucial for institutional participation. However, due to the throughput limitations of early blockchains, implementing performant on-chain order books was not feasible. This led to the dominance of AMMs in early DEX design.

AMMs, which rely on liquidity pools and algorithmic pricing formulas (often supported by oracles), are simple and accessible. They are well-suited for launching new or niche tokens that wouldn’t naturally attract liquidity in an order book model. Raydium, for example, leveraged AMMs to bootstrap trading for meme coins and other emerging assets within Solana’s ecosystem.

Yet, this simplicity comes at a cost. AMMs struggle with capital efficiency and trade execution for larger or more complex orders. Slippage can be significant, and liquidity providers face risks from MEV (Miner Extractable Value) and oracle-driven pricing delays. While AMMs excel at powering basic swaps—as seen with Uniswap—they are fundamentally incompatible with high-performance trading strategies. This makes AMMs particularly inadequate for both perpetual futures and blue-chip spot trading, where speed, precision, and capital efficiency are paramount.

The Structural Mismatch in Crypto Liquidity

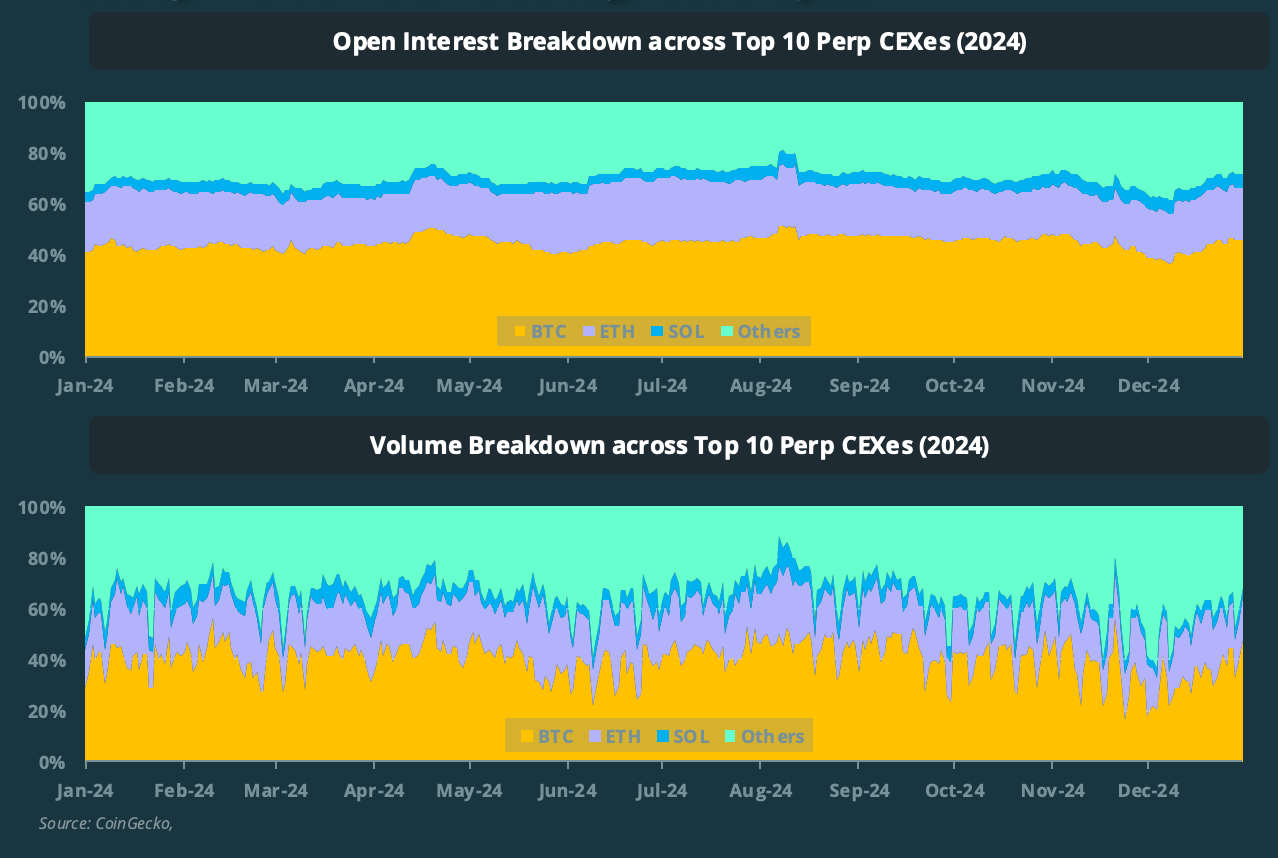

The limitations of AMMs are especially apparent when you consider the structure of crypto trading itself. Crypto markets are top-heavy, dominated by blue-chip assets like BTC, ETH, and SOL, which collectively account for more than two-thirds of total trading volume. And this volume is overwhelmingly driven by institutional participants who demand robust infrastructure: low latency, deep liquidity, and accurate pricing.

This creates a structural mismatch. Centralized exchanges continue to dominate institutional trading because non-order-book DEXs simply can’t meet the performance demands of their largest users. As a result, decentralized perpetuals and blue-chip spot markets have significantly lagged. This has left a massive, persistent infrastructure gap in DeFi—particularly on the derivatives side—one that Hyperliquid was purpose-built to fill.

How Hyperliquid Rebuilt the DEX from the Ground Up

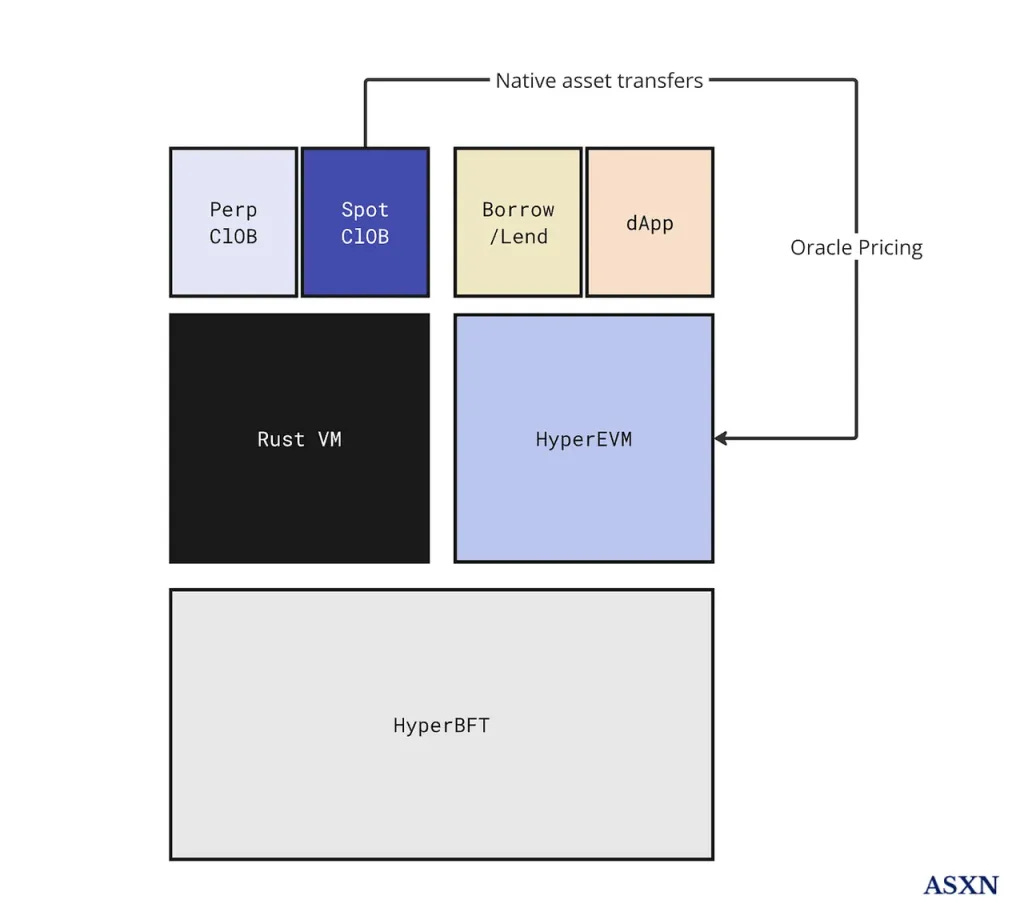

To build a professional, institutional-grade trading platform, Hyperliquid didn’t start by launching a Layer 1 blockchain—it started with the product. The team launched its perps exchange first to find product-market fit, and only later revealed that it was already running entirely on a custom proof-of-stake Layer 1 blockchain—powered by the HyperBFT consensus and RustVM execution layer, capable of reaching up to 2 million transactions per second.

At its core is a custom Central Limit Order Books (CLOBs), a matching engine that pairs buy and sell orders in real time, delivering the speed and precision needed for high-frequency, on-chain trading. This architecture eliminates reliance on Ethereum, Solana, or Layer 2 solutions and redefines performance standards for decentralized exchanges.

In addition to its on-chain order book, Hyperliquid introduced Market-Making Vaults (MMVs)—infrastructure built on top of its CLOBs—that allow users to pool USDC and passively earn from market-making, trading fees, and funding payments. Vault managers earn 10% of the profits but must stake 5% of the vault’s assets. The flagship vault, HLP, operated by Hyperliquid, delivered a 50% return in 2024.

More than just a market-making yield product, HLP played a crucial strategic role: it allowed founder Jeff Yan to bootstrap early liquidity on the platform. Thanks to his prior market-making experience at Hudson Trading Group and his own firm, Chameleon Trading, Jeff was uniquely positioned to bootstrap the system in a way few others could. Importantly, MMVs democratize on-chain market making, a role previously reserved for major players like Citadel in traditional finance.

Just as importantly, Hyperliquid is built with a non-custodial design—meaning the exchange cannot access or move user funds. This was a deliberate architectural decision, shaped in part by the collapse of FTX, which left a lasting impression on him and reinforced a core belief: users should always retain full control of their assets.

The result wasn’t just a better product—it was market expansion. Hyperliquid didn’t simply steal share from dYdX and GMX, which relied on off-chain order books and AMM-style liquidity, respectively. It solved the deeper challenge: previous protocols compromised either on performance (GMX) or on decentralization and composability (dYdX). By delivering the first fully on-chain order book with CEX-level speed and precision, Hyperliquid accomplished what others could not:

- Pulled volume from centralized exchanges

- Onboarded institutional and professional traders into DeFi

- Reshaped the decentralized perps landscape and unlocked new demand

In doing so, Hyperliquid filled a critical gap in DeFi: a perps-native platform that combines full decentralization with pro-grade execution. And if spot adoption is any indication, decentralized perps are still in the early innings. Looking ahead, Hyperliquid’s next two major opportunities lie in the broader Layer 1 ecosystem and—perhaps most under-appreciated by analysts—spot trading, a segment poised for significant growth.

Expanding Beyond Perps: Hyperliquid’s Spot Trading Breakout

After initially launching their perpetuals, Hyperliquid launched their spot product in March 2024 with the same on-chain order books model and fee schedule. Initially, it was only a few asset pairs, but has quickly grown to list numerous assets that are minted on Hyperliquid via the HIP-1 auction process. However, unlike the Solana ecosystem where minting a token is low cost, there is a listing fee in the Hyperliquid ecosystem, which limits spam tokens and encourages serious projects.

To enhance interoperability across the broader crypto ecosystem, the Hyperliquid platform has integrated with Hyper Unit—a decentralized protocol developed by Shoku and team for asset tokenization and bridging. With Hyper Unit, users can deposit external assets like BTC or ETH and receive tokenized equivalents (e.g., uBTC) on HyperCore. Previously, Hyperliquid only supported USDC. By using distributed validation instead of centralized custodians, Hyper Unit enables secure, trustless cross-chain transfers into the Hyperliquid ecosystem.

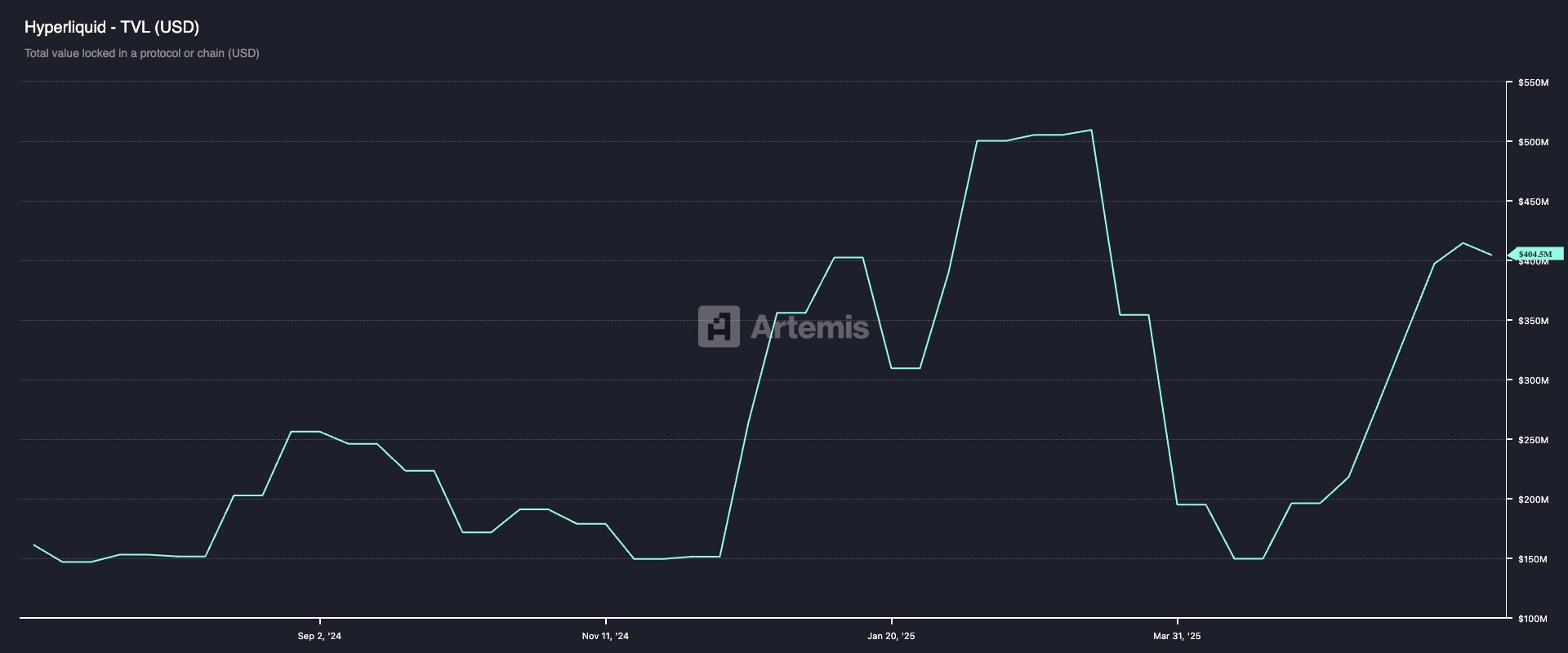

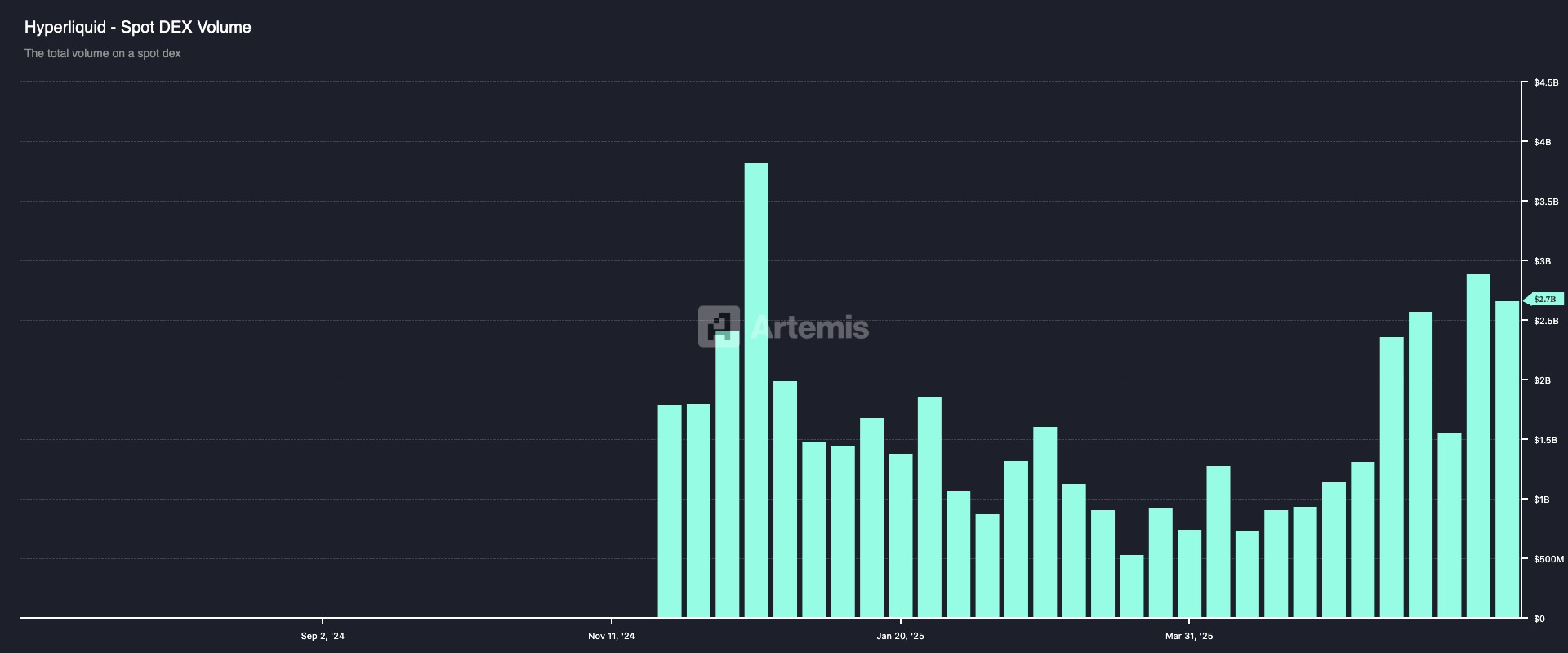

Since its launch, spot trading volume on Hyperliquid has surged to levels near its all-time highs from December, even while major centralized exchanges (CEXs) remain at only 50% of that peak. This divergence appears to be driven by whales from BTC, ETH, and SOL ecosystems bridging assets into Hyperliquid to execute trades, then bridging back out. As a result, while trading volume has grown meaningfully, total value locked (TVL) has remained relatively flat.

Hyper Unit may be quietly powering one of the most underappreciated narratives in the Hyperliquid ecosystem: a spot market breakout enabled by the performance of on-chain central limit order books (CLOBs).

Hyperliquid’s Layer 1 Flywheel: From Exchange to Ecosystem

Following the launch of its SPOT market, Hyperliquid introduced a points-based incentive program to boost trading ahead of its token release. Running from early to mid-2024, the program helped Hyperliquid capture a growing share of on-chain perpetuals trading. On November 29, 2024, it launched its native token, HYPE, airdropping 31% of the 1 billion supply to early users. The airdrop sparked strong community engagement and sustained trading momentum—unlike other protocols that saw activity drop after incentives ended.

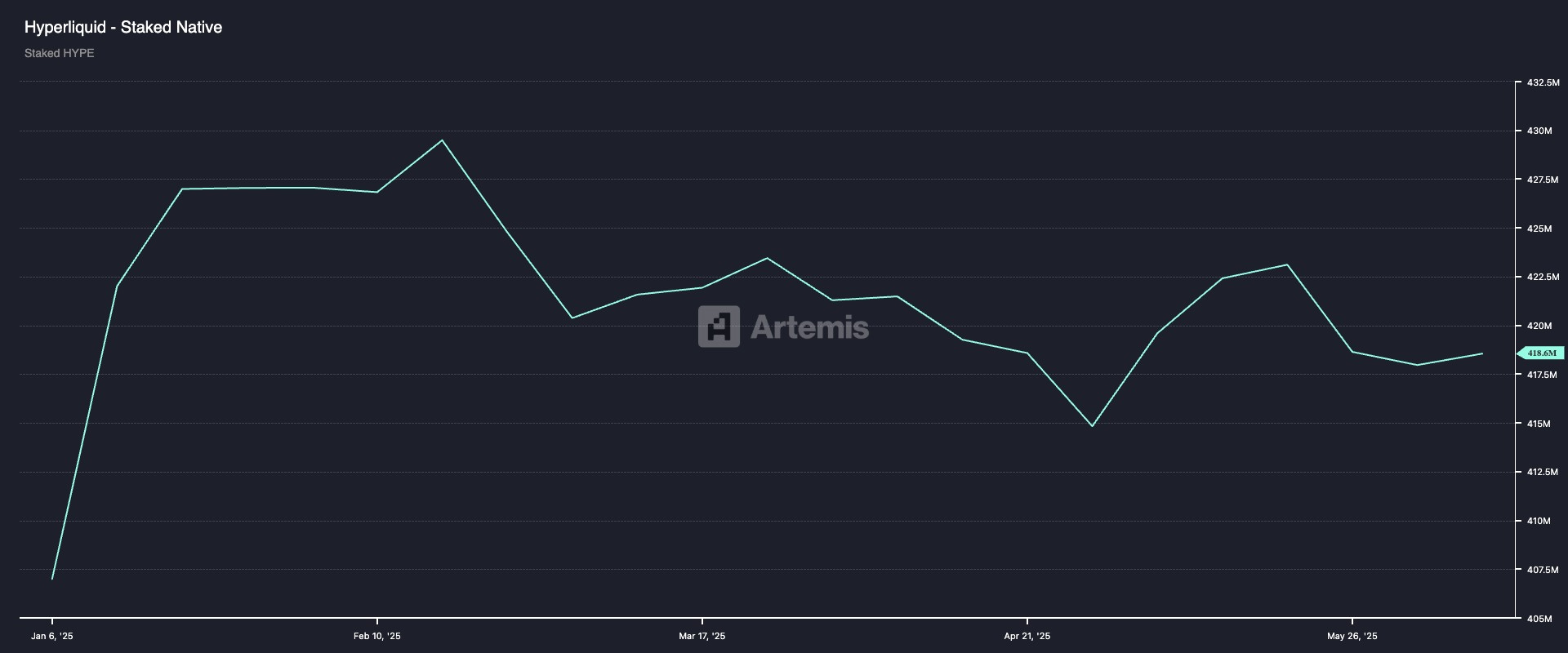

Next, the month after the token launch, Hyperliquid enabled HYPE staking to secure its Proof-of-Stake (PoS) network. HYPE holders could earn an annual yield of approximately 2.5% as a staking reward.

Lastly, on February 18, 2025, Hyperliquid launched HyperEVM, transforming into a general-purpose Layer 1 capable of hosting third-party smart contracts and DeFi apps. The exchange now runs on HyperCore (RustEVM), while HyperEVM supports DeFi—both secured by the unified HyperBFT consensus. Integration is seamless; EVM contracts can interact directly with the exchange. HyperCore has no gas fees, and HyperEVM offers low fees for DeFi. While the exchange remains the core driver of liquidity and users, HyperEVM expands Hyperliquid’s reach across the broader DeFi ecosystem.

We believe HyperEVM has a strong likelihood of success. At its core, DeFi exists to unlock liquidity and leverage—but most ecosystems struggle to generate organic demand for either. Hyperliquid’s exchange provides a natural foundation for both, making it an ideal catalyst for sustainable, demand-driven growth. As a result, we expect the Hyperliquid ecosystem to expand rapidly and organically.

As Jeff puts it, the strategy is to “polish a native application and then grow into general-purpose infrastructure”—not the other way around.

The HyperEVM Ecosystem: Early Indicators of a Thriving DeFi Landscape

Since the launch of HyperEVM earlier this year, its total value locked (TVL) has rapidly surpassed $1 billion in just a few months—a remarkable pace of growth. To assess the overall state of the Hyperliquid ecosystem, we examine key indicators such as decentralized exchanges (DEXs), liquid staking, lending protocols, and stablecoin adoption.

Decentralized Exchange:

Built on HyperEVM, Hyperswap is the leading AMM-based DEX in the Hyperliquid ecosystem, surpassing $70M in TVL and $2B in volume within just four months. It serves as a critical launchpad for new and experimental tokens.

While Hyperliquid’s CLOBs delivers deep liquidity for its spot markets, bootstrapping liquidity for long-tail assets has still proven challenging. This is where AMMs shine. Hyperswap offers permissionless listings, dramatically lowering the barrier to entry for long-tail tokens. Its AMM model provides automated liquidity without the need for active market-making or order book management.

This makes Hyperswap ideal for early-stage projects looking to gain traction and build community. Over time, successful tokens may “graduate” to Hyperliquid’s CLOBs, accessing deeper liquidity and more active trading. In this way, Hyperswap functions like the U.S. pink sheets—an incubator for emerging assets that eventually feed into more established markets.

Liquid Staking:

StakeHyper is the leading liquid staking platform on Hyperliquid. It enables users to stake smaller amounts and receive stHyper, which allows them to remain liquid while staking. Currently, the platform has a total value locked (TVL) of $464.86 million, with 11.4 million HYPE staked. The current annual percentage yield (APY) is 2.1%.

Lending/Borrowing:

HyperLend, often known as “the Aave of Hyperliquid,” is the ecosystem’s first lending protocol—enabling overcollateralized borrowing with dynamic rates and real-time interest accrual. Built independently by the community, HyperLend plays a key role in expanding leverage, unlocking HYPE yield opportunities, and boosting capital efficiency. Since its April launch, it has surpassed $350M in TVL and $100M in active loans, mirroring Aave’s early growth trajectory.

Stablecoins:

In mid June, Hyperliquid’s stablecoin ecosystem introduced USDhl, a fiat-backed stablecoin from Felix Protocol. Backed 1:1 by short-term U.S. Treasuries, USDhl redirects its yields to buy back HYPE and reward DeFi activity—aligning ecosystem growth with tokenholder value. Rewards are split between HyperCore traders and HyperEVM LPs and lenders, making USDhl both a stable asset and a native incentive engine for the Hyperliquid ecosystem.

Overall, we’re beginning to see HyperEVM and its ecosystem take shape relatively well, though it's still early. We’re excited to see continued development in the space.

HIPs: The Blueprint for a Permissionless Financial System

HIPs—short for Hyperliquid Improvement Proposals—are on-chain governance proposals that define how the protocol evolves over time. Each HIP introduces a concrete, community-ratified change to Hyperliquid’s functionality or structure, often reflecting broader shifts in vision, capability, or market strategy.

HIP-1, HIP-2, and HIP-3 aren't just technical upgrades—they're strategic steps toward Hyperliquid’s long-term vision: a fully decentralized, performant financial platform with protocol-native liquidity and community-led expansion. Together, these proposals define a new operating model for how assets are listed, how liquidity is provisioned, and how new markets are launched.

They mark Hyperliquid’s evolution from a high-performance DEX into a permissionless, scalable platform—one where infrastructure is shared, incentives are aligned, and innovation is composable. Understanding these HIPs is key to understanding where Hyperliquid is headed—and why it might lead the next wave of DeFi adoption.

HIP-1: Governance-Driven Listings for Quality Assets

While Hyperswap enables frictionless, permissionless access to liquidity, HIP-1 introduces a more selective, protocol-native path for listing assets on Hyperliquid’s CLOBs-based spot exchange. HIP-1 (short for Hyperliquid Improvement Proposal 1) is a governance proposal passed by the community that defines how new tokens—especially those denominated in HYPE—can be listed through a bidding process using the HYPE token.

This model helps surface quality projects, but it also raises the barrier to entry—especially for newer tokens lacking deep liquidity or financial backing. And while the CLOBs model excels in mature markets, it's less effective for bootstrapping liquidity, a limitation that has hindered the growth of many HYPE-based pairs under HIP-1.

HIP-2: On-Chain Liquidity, Automated and Decentralized

To address this gap, the Hyperliquid protocol introduced HIP-2 in April 2024—a novel, protocol-native liquidity engine that automates the creation of tightly spaced limit orders (0.3% spread) directly on the spot order book. HIP-2 mimics AMM-like passive liquidity behavior through a grid of limit orders, but it operates fully within the CLOB model. This lets token deployers bootstrap deep, permissionless liquidity without relying on off-chain market makers or facing the risks of LP rug pulls. Liquidity is locked on-chain and fully transparent.

In March 2025, HIP-2 was fully decentralized, removing all team-run validators and integrating directly into the Layer 1 consensus. This move established autonomous, trustless liquidity provisioning, a first at Layer 1 scale. The decentralization significantly boosted confidence among users

HIP-3: Turning Hyperliquid into a Trading Market Creation Engine

HIP-3 is a pivotal upgrade that transforms Hyperliquid into a platform for building platforms—enabling permissionless perpetuals much like Uniswap did for spot markets. By making liquidity a protocol-level feature, HIP-3 allows anyone to launch perp markets for long-tail assets, a key driver of DEX growth.

Builders can stake 1 million HYPE (individually or via multisig) to join a Dutch auction for a deployment slot, replacing flat listing fees with a demand-driven model. Once approved, they control market parameters—such as oracles, leverage, and funding—while earning up to 50% of base trading fees, with options for custom fees and frontends.

To ensure security and accountability, mismanaged or exploited markets risk having builder stakes slashed via validator governance.

In general, HIP-3 opens the door to:

- Niche or long-tail assets

- Legally sensitive markets the core team cannot list

- Non-crypto perps

HIP-3 doesn’t just add new markets—it unlocks decentralized market creation at scale, fueling Hyperliquid’s next phase of volume growth.

Where Value Flows: HYPE vs. HLP

At the core of the Hyperliquid ecosystem are two key tokens: HYPE and HLP.

- HYPE is the protocol’s native token. It captures value from trading fees, staking, and Layer 1 gas fees. Holding or staking HYPE aligns you with the success of the full ecosystem.

- HLP is the liquidity provider token. It earns yield from market-making profits and funding fees but does not participate in protocol revenue.

In short, HYPE is a directional bet on Hyperliquid’s long-term growth, while HLP is a non-directional bet on trading volume and market-making efficiency.

To understand where value accrues, it helps to separate three key flows:

Exchange Business

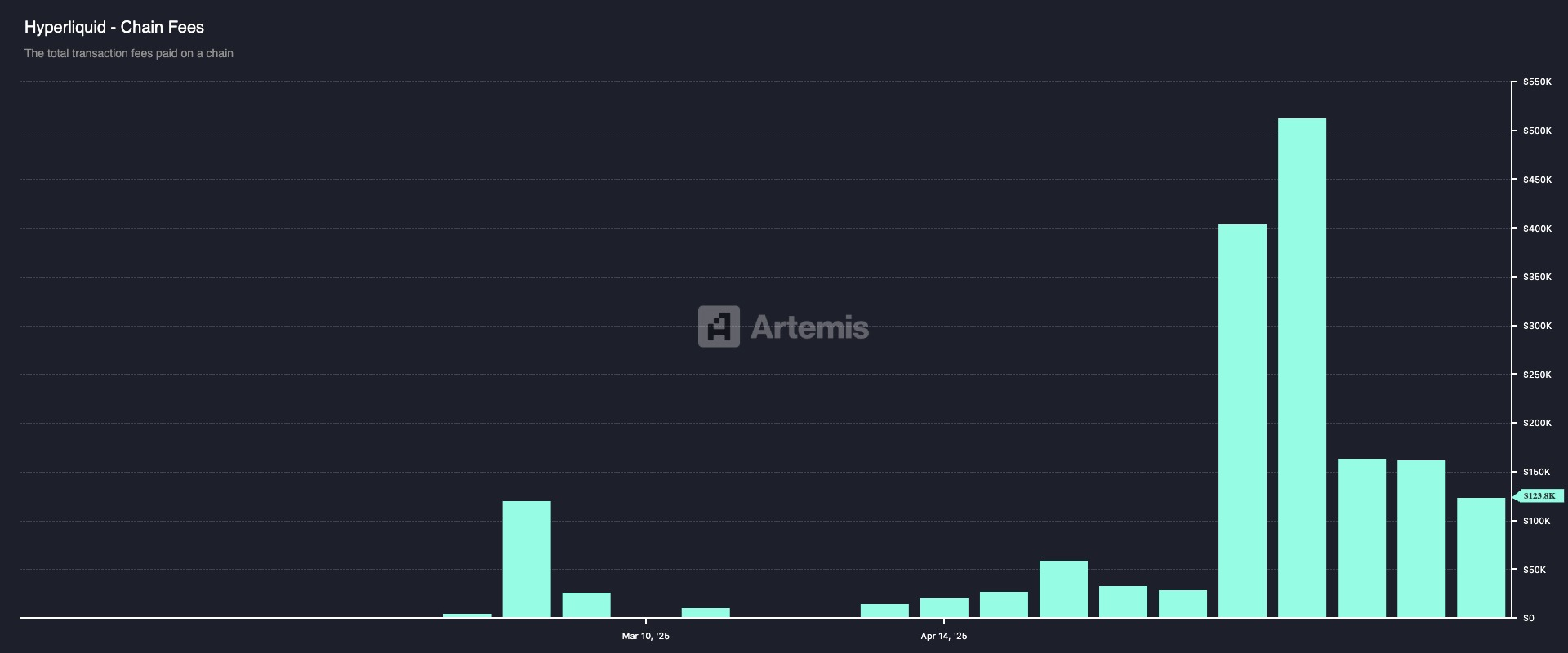

- Trading Fees (Spot & Perpetuals): The primary source of revenue is trading fees. Hyperliquid mirrors Binance’s fee structure, using a maker-taker model with tiered rates based on 14-day trading volume. For spot markets, fees denominated in non-USDC are automatically burned—reducing circulating supply and enhancing long-term token value.

- Liquidation Fees: Collected when leveraged positions are closed and passed to the liquidator vault.

- HIP-1 Auction Fees: New token listings are auctioned in USDC, with proceeds going to the protocol.

HyperEVM

- Currently, Hyperliquid’s main trading platform does not charge gas fees. However, transactions on the HyperEVM require HYPE for gas, and these fees are burned. HYPE stakers earn emissions at an annual rate of approximately 2.5% and receive discounts on trading fees.

How does HLP make money?

- Derivative Funding Fees: When traders open perpetual contracts, they pay continuous funding fees to keep the contract price aligned with the index price. The HLP vault accrues this value directly.

- Spread and Market Making Fees: The main source of revenue for HLP comes from bid-ask spread capture and trading PnL. Hyperliquid as a protocol does not charge spread fees.

HYPE: A Token Built for Alignment, Scarcity, and Growth

The tokenomics of $HYPE set a new benchmark in protocol design. With a fixed 1 billion token supply and no inflation, HYPE ensures long-term scarcity. Its fee structure is highly user-aligned: 97% of trading fees go to the Assistance Fund to buy back HYPE, while only 3% supports liquidity providers in the HLP vault—making it one of the few protocols that channels nearly all revenue back to the token.

Furthermore, its community-first distribution model has attracted loyal users. With zero allocation to venture capital and 70% of the total supply reserved for users, the project embodies the ethos of decentralized ownership. The token distribution at launch was as follows:

- 31.0% – Airdrop to Early Users: Immediately liquid, rewarding active traders and early adopters

- 38.888% – Community Emissions: Reserved for future incentives (trading rewards, liquidity mining, referral bonuses, etc.)

- 23.8% – Team (Core Contributors): Locked for one year, with gradual vesting mostly between 2027–2028

- 6.0% – Hyper Foundation: For ecosystem grants, infrastructure, and validator staking

- 0.3% – Community Grants: To support builders, developers, and key partners

- 0.012% – HIP-2 (Hyperliquidity): A micro allocation tied to an experimental liquidity incentive

At its Token Generation Event (TGE), Hyperliquid airdropped 31% of HYPE to over 100,000 users, instantly creating thousands of new millionaires and catalyzing a vibrant, engaged community. Rather than exiting, many recipients stayed—becoming core users and evangelists. It’s a prime example of Web3 done right: users becoming owners, aligned to grow the network they helped build.

This alignment fuels a powerful flywheel: as HYPE appreciates, it draws more users; those users generate fees; the protocol buys back HYPE with those fees—driving price and reinforcing growth. Crucially, this happens without inflation. As Hyperliquid’s ecosystem expands—with DeFi apps like USDhl contributing to buybacks—the flywheel strengthens further, compounding adoption, liquidity, and long-term value accrual.

The first core contributor unlock begins in November 2025, vesting through 2027. While the 38.88% community emission plan is still to be detailed, the total HYPE supply remains capped at 1 billion.

Key Risks: What Could Derail the Hyperliquid Thesis

Hyperliquid faces five major risks that could significantly impact its long-term trajectory.

- Protocol-level KYC/AML enforcement: Hyperliquid’s rapid growth has been largely driven by non-KYC users trading decentralized perpetuals—often from jurisdictions where such activities are lightly regulated or untaxed. Introducing mandatory KYC/AML requirements at the protocol level could severely dampen adoption and undermine one of the platform’s core value propositions: permissionless, non-custodial trading.

- However, Hyperliquid differs from traditional exchanges in that it is non-custodial by design—it never holds user funds or facilitates settlement directly.

- The introduction of builder codes which allowes users to build front-ends on top of Hyperliquid’s orderbook engine, supports a modular compliance strategy. They can allow third-party frontends to implement KYC if needed, thus bridging regulatory obligations with the protocol’s decentralized foundation—without compromising its neutrality.

- Increased Competition: Both Coinbase and Robinhood have recently announced futures products for their users, signaling intensified competition in the space. A significant portion of Hyperliquid’s user base is based in the U.S., where these platforms have strong reach.

- However, it remains unclear how effectively Robinhood and Coinbase will be able to bootstrap liquidity. Currently, Robinhood and Coinbase offer only 3x and 5x leverage, respectively, for their users—whereas Hyperliquid offers up to 40x. The growing demand for decentralized platforms, driven in part by tax advantages, may also limit their ability to capture meaningful market share from Hyperliquid. Rather than acting as direct competitors, Coinbase and Robinhood may ultimately help expand the overall addressable market by on-ramping more U.S. users into the world of perpetuals trading.

- Vault Risk: Exploits and arbitrage vulnerabilities in HLP: The decentralized HLP vault is vulnerable to arbitrage and manipulation, as seen in the JELLY incident. Sophisticated actors can exploit discrepancies in funding rates or pricing logic, which may result in systemic leakage of value. As the platform scales, robust risk management and greater transparency will be critical.

- Validator Centralization: Although Hyperliquid brands itself as decentralized, its validator set remains relatively concentrated. This introduces risks to censorship resistance and network-level security.

- That said, validator decentralization, as seen with Solana, can improve over time.

- Smart Contract Risk: As with all on-chain systems, Hyperliquid is exposed to the risk of critical bugs or exploits in core components—including the perpetuals engine, vault system, or cross-chain bridging infrastructure. A significant flaw could lead to catastrophic losses or downtime, eroding user trust and halting protocol operations.

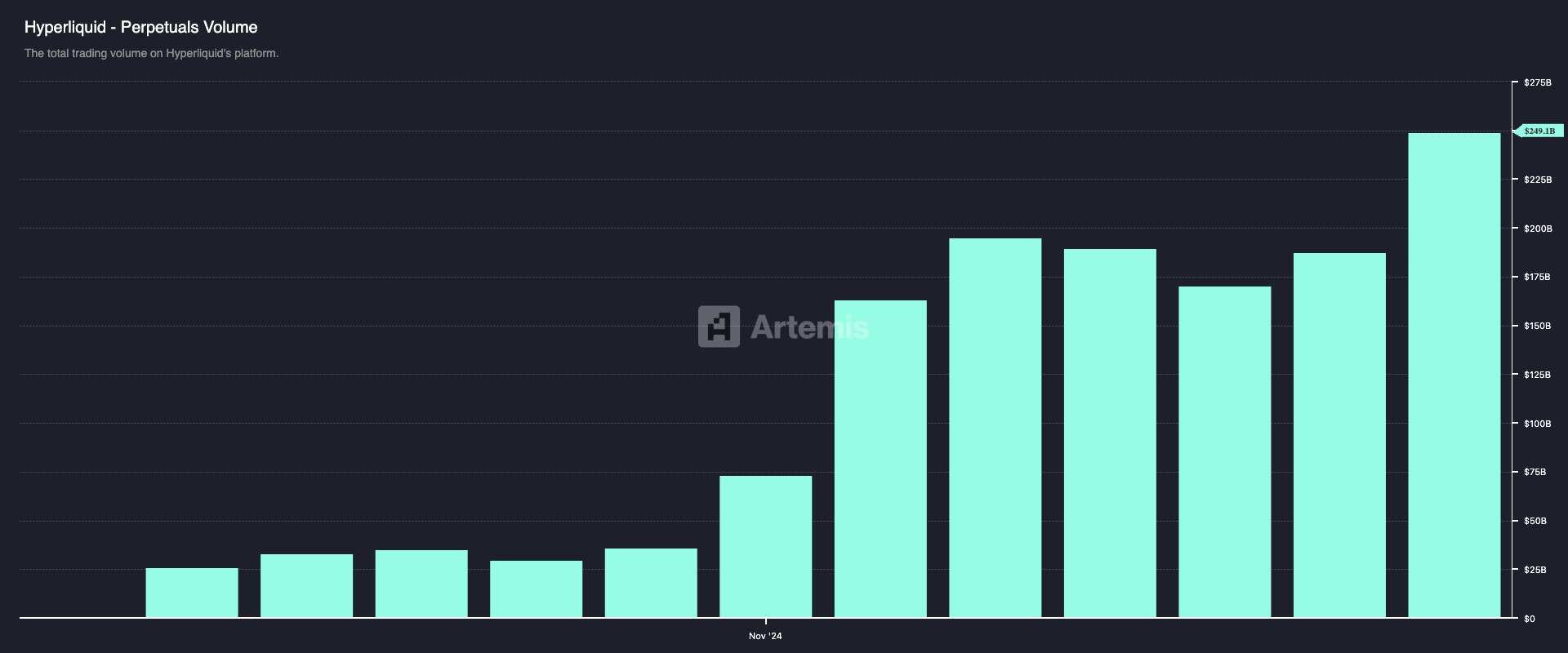

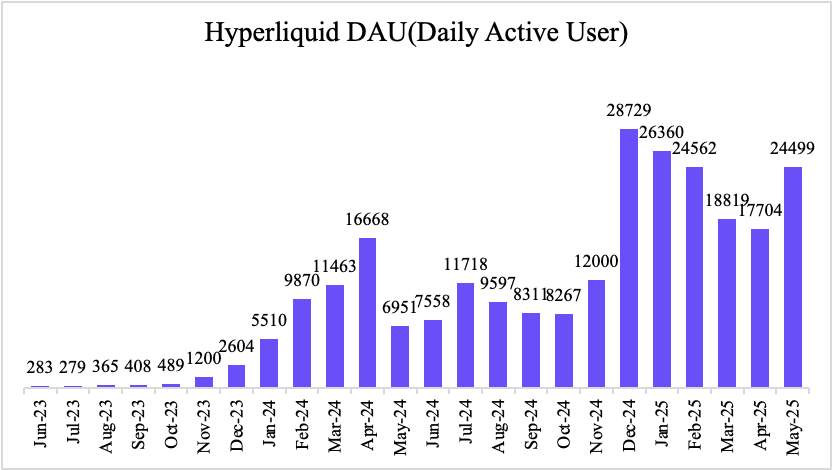

By the Numbers: How Hyperliquid Is Outpacing the Market

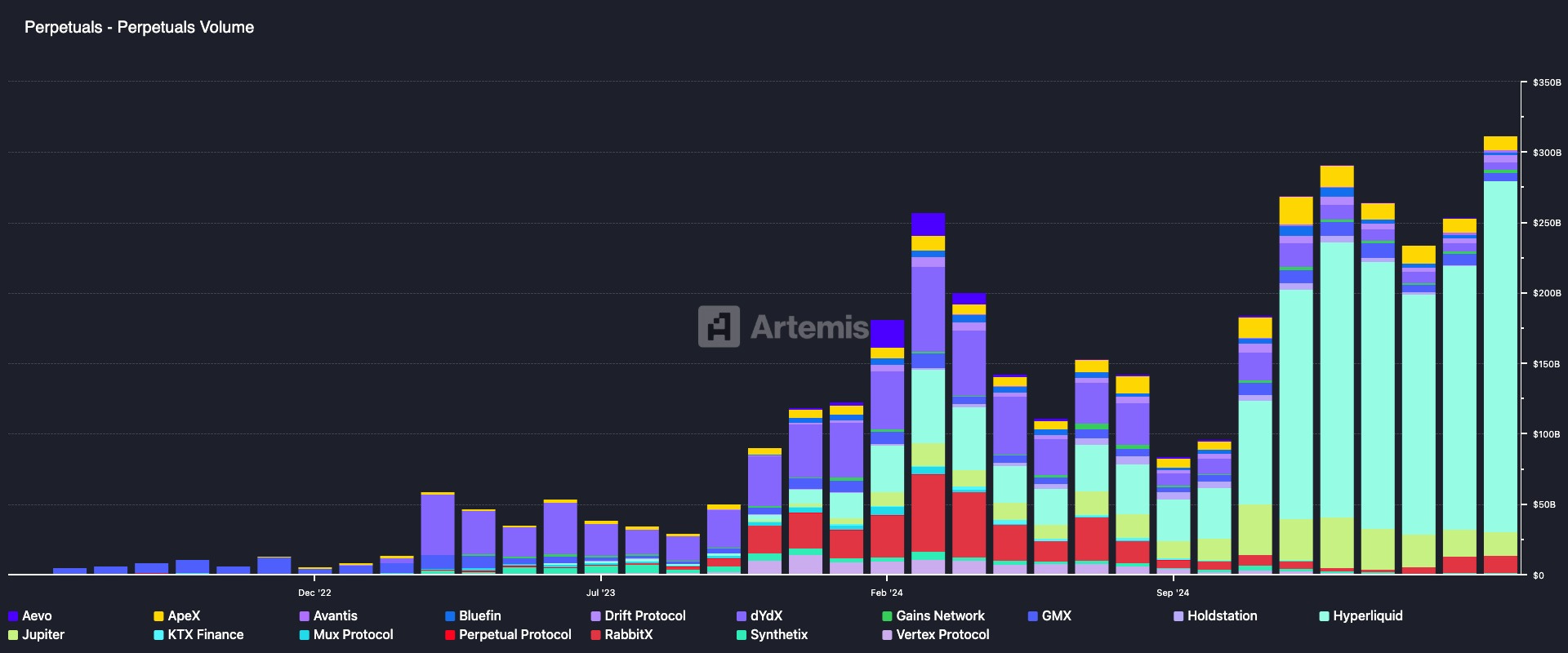

Hyperliquid’s growth has been extraordinary, with trading volume soaring from $1 billion in June 2023 to over $250 billion by May 2025—a 3.5× increase since its Token Generation Event (TGE).

Moveover, in 2025, the platform is averaging $55 million in monthly revenue (calculated as 97% of fees).

In parallel with volume growth, daily active users (DAUs) have expanded from 283 to over 20,000. Remarkably, as previously mentioned, this growth has persisted post-TGE and post-farming season, signaling genuine user retention and organic adoption—a rare outcome in crypto markets that are often dependent on short-term incentives.

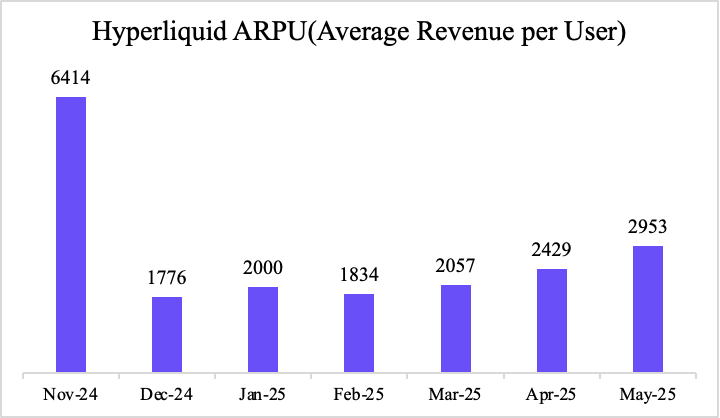

Since December 2024, Hyperliquid’s average revenue per user (APRU) has also risen significantly, increasing from $1,776 to over $2,953 monthly, reflecting improved monetization and user stickiness.

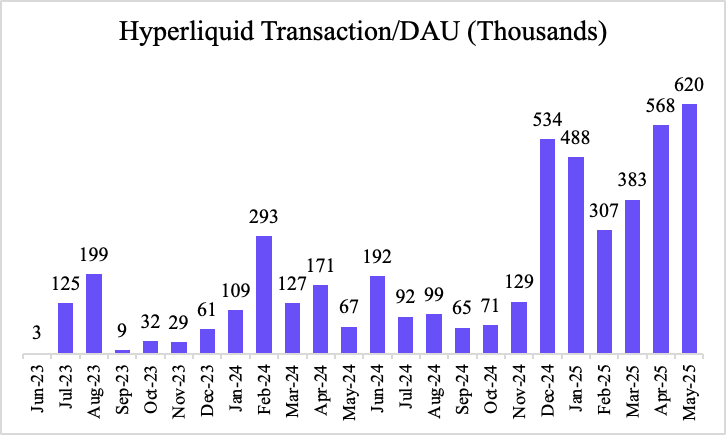

This trend is further reinforced by growth in monthly volume and transaction counts per user. Since the TGE:

- Volume per DAU has doubled, as has the number of transactions.

- Average monthly volume per user is now close to $10 million.

- The platform sees over 600,000 monthly transactions per user.

These metrics suggest a shift toward professional and algorithmic trading behavior, rather than purely speculative retail activity.

Another telling signal of this shift is the average volume per transaction, which has declined from over $100 in 2023 to below $20 in 2025. While this might seem negative at first glance, it reinforces growing algorithmic activity—smaller, more frequent trades often linked to quant strategies. Importantly, despite the drop in trade size, both overall volume and user count have grown, validating this as healthy, infrastructure-level adoption.

Finally, throughout this growth phase, Hyperliquid’s take-rate has remained stable, confirming that platform expansion is driven by organic demand rather than fee structure manipulation.

Valuing Hyperliquid: A Sum Of The Parts (SOTP)x Approach

We assess Hyperliquid’s fair value under both bear and bull cases by segmenting its business into two components:

- Exchange business (Perpetuals, Spot, HIP-1)

- Layer 1 (HyperEVM)

To determine a fair valuation range for the Exchange segment, we reference 2025 consensus P/E multiples from comparable public companies—specifically, Coinbase and Robinhood. Using their projected net income and market capitalizations, we derive a valuation range of $48.81–$50.60 billion for HyperCore based on Coinbase and Robinhood’s PE Multiple.

For HyperEVM, valued as a Layer 1 protocol, we benchmark against Solana and Ethereum using a Fully Diluted Valuation (FDV) to Fees multiple. Based on annualized fee data derived from the most recent complete month, we estimate a valuation range of $2.24–$9.02 billion for HyperEVM based on Solana and Ethereum’s Fees/FDV Multiple.

To derive the overall fair value range, we add the lower-end estimates of the exchange and Layer 1 segments for the bear case, and the higher-end estimates for the bull case:

Based on the results and the current price of ~40 (as of 06/30/25), I believe Hyperliquid is undervalued under this sum-of-the-parts framework.

Why Hyperliquid Breaks the Tradition Valuation Methods

While the sum-of-the-parts (SOTP) framework provides a solid valuation floor, the bigger pictures lies in Hyperliquid’s exposure to:

(1) The high-growth trajectory of decentralized perpetuals

(2) The monopolistic nature of decentralized perps- where winner takes all

(3) The fact that HYPE is a high-growth, high-buyback asset.

Looking ahead, the DEX-to-CEX perps ratio may begin converging with that of spot trading—fueled by rising demand for no-KYC trading, builder codes, and long-tail and non-crypto (equities) perp listings via HIP-3. If this plays out, perp volume could at least 3x from current levels, implying a 32.1% CAGR.

More importantly, DEX perps are structurally more monopolistic than CEXs. In centralized markets, share shifts are often driven by regulatory crackdowns or geographic fragmentation—not superior product. In contrast, decentralized perps operate in a borderless, permissionless environment, where dominance is determined by liquidity and user experience. This enables a powerful compounding flywheel for the market leader.

With ~70% market share, Hyperliquid is well-positioned to maintain dominance. If sustained, HYPE buybacks could grow at a 32.1% CAGR—potentially faster when accounting for spot trading and HyperEVM burn.

Traditional valuation frameworks miss what makes Hyperliquid special. In TradFi, companies are usually either:

- Value stocks: Slower growth, but return capital via buybacks/dividends.

- Growth stocks: Rapid expansion, little or no buybacks.

Hyperliquid is a rare hybrid—delivering rapid growth and returning capital via buybacks.

To put in persepctive, we compared Hyperliquid to the MAG5. On average, MAG5s trades at 37x buyback + dividend yield, with 15.64% net income growth. Hyperliquid, with ~150% expected 2025 net income growth, is trading at a multiple between Nvidia and Microsoft.

Conclusion: Hyperliquid’s Growth Is Just The Beginning

Hyperliquid has rapidly evolved from a high-performance perps exchange into a full-fledged DeFi ecosystem. By combining CEX-grade execution with fully on-chain infrastructure, it has captured dominant market share in decentralized derivatives and laid the groundwork for sustainable, user-aligned growth.

With the launch of HyperEVM, liquid staking, lending, and protocol-native stablecoins, Hyperliquid now offers a vertically integrated platform—powered by real usage, not just incentives. Its unique model defies traditional trade-offs and creates a powerful flywheel of liquidity, adoption, and value accrual.

If current momentum continues, Hyperliquid may not just lead DeFi’s next wave—it may become the standard for how crypto ecosystems are built.

Disclosure: The authors of this content, as well as affiliates of Artemis Analytics, may have financial interests in the protocols or tokens mentioned. This does not constitute investment advice or a recommendation to buy, sell, or hold any asset. The information provided is for educational purposes only and should not be relied upon for financial, legal, or tax decisions. Readers should assess their own circumstances before making any financial choices. Views expressed may change without notice, and Artemis Analytics is not liable for any losses resulting from the use of this content.