.webp)

Hey Fintech / Crypto Investors,

Welcome back to another weekly fundamental from a former VC and HF analyst who takes a no-BS lens into blockchains, protocols, fintechs, DATs, stablecoins, etc.

What a week.

1. Crypto Equity Acquisition

Echo gets acquired for $375M and MegaETH raises $600m with 1 day and 17 hours left in an 11.9x+ oversubscribed ICO via Sonar by Echo pinning MegaETH at $11b FDV.

While the headline could be ICOs are back and token businesses can raise a lot of money at large valuations, the Echo acquisition by Coinbase made me wonder again if the value is accruing to equity versus tokens this cycle —

- Circle trades at $35B (pre IPO they were in talks for a $5B round so this is a quick 7x)

- Tether is worth $500B

- Ripple acquired Hidden Road for $1.25B

- Fortune reports that BVNK may be acquired for $2B

- This doesn’t even account for both Stripe’s acquisition of both Privy (rumored at $500m) and Bridge ($1.1B)

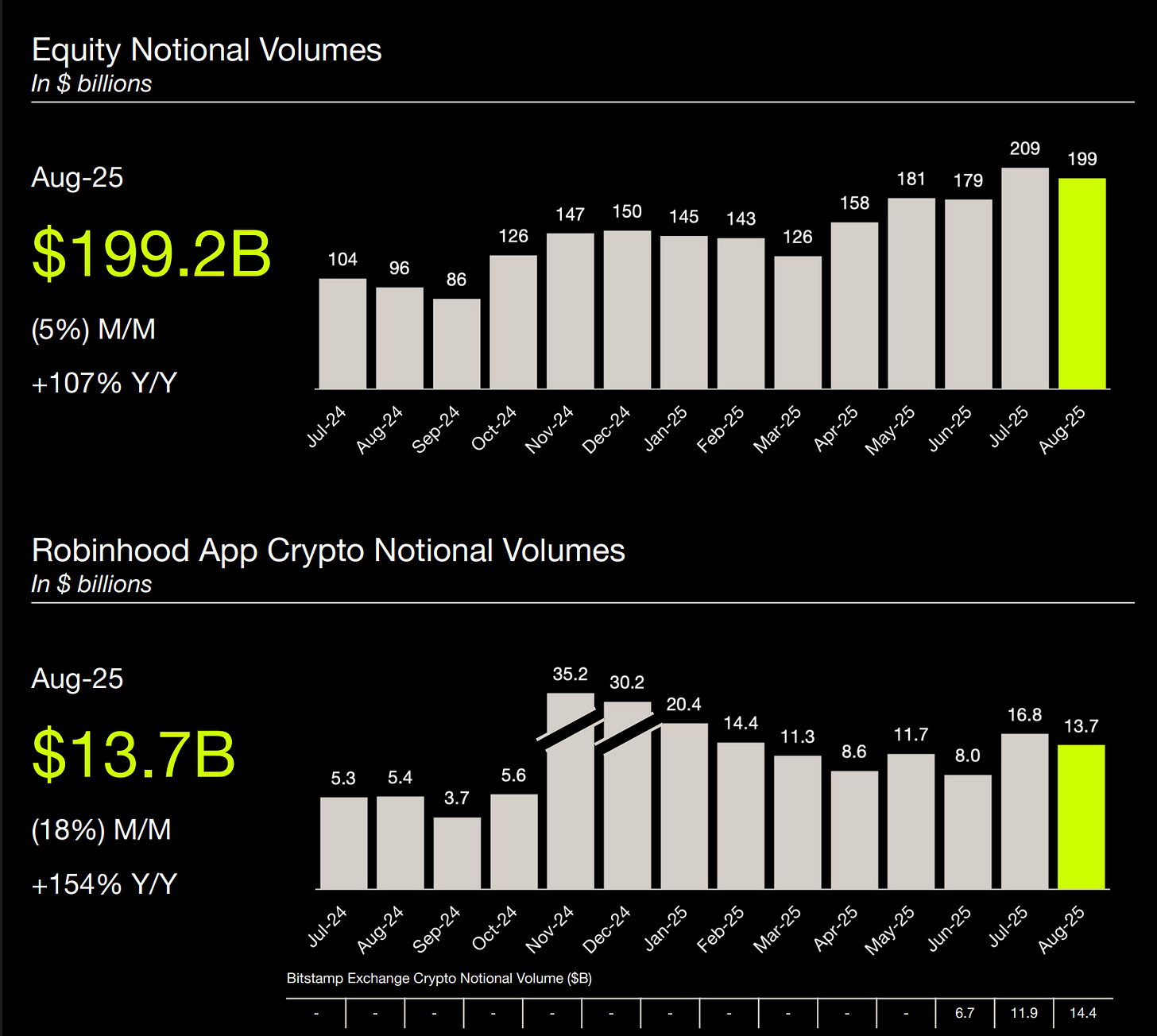

Remember Robinhood is the biggest winner of the tokenization / stablecoin / prediction market / DAT meta — Robinhood is up 425% in the last year whereas BTC / ETH are sitting at 60% up in the last year and this is pre Trump election.

Robinhood is absolutely crushing it on the equity and crypto trading volume as a non token business:

We will continue to see big winners among tokens with Hyperliquid as the clear darling with $6B of FDV at TGE and now sitting at $48B of FDV and $1.2B annualized revenue (buybacks from trading fees, chain fees)— an 8x that anyone could’ve invested in liquid public markets.

However, I think the struggle for tokens (both chains and protocols) vs equities are two fold:

- How do we value blockchains? Its not clear, the revenue multiples are all over the place and there isn’t consensus on if its REV, TVL, Revenue, Fees, Application Revenue, Total Economic Activity, etc. As an industry, we need to align on what is FCF, earnings, revenue multiples for blockchains.

- There needs to be more transparency on cap table: I’ve heard informally from multiple sources and investors and teams, holders dumping at TGE or OTC or getting revenue indirectly through staking rewards. Its hard for a large financial institution to buy a token and have a token crash 80% and not knowing if it was a market maker, team insider selling and dumping, or some other reason. In equities we have 13-Fs and clear disclosures when management, investors, or large holders sell. Without clarity and clear information asymmetry (Felipe at Theia talks about this in much more depth), tokens will trade at a discount to equities until tokens become equity-like with clear token holder protections.

- Investor Relations / Quarterly Earnings Calls: until we get protocols and blockchains GUIDING to what KPIs they are growing, what are expectations and reporting on progress each quarter, the market will trade on narrative / momentum and news. Kudos to Maple, EtherFi, Jupiter, among others for kicking off consistent quarterly earnings calls and disclosing KPIs and financials.

I argue below that DePin protocols likely trade the closest to Web 2 technology businesses.

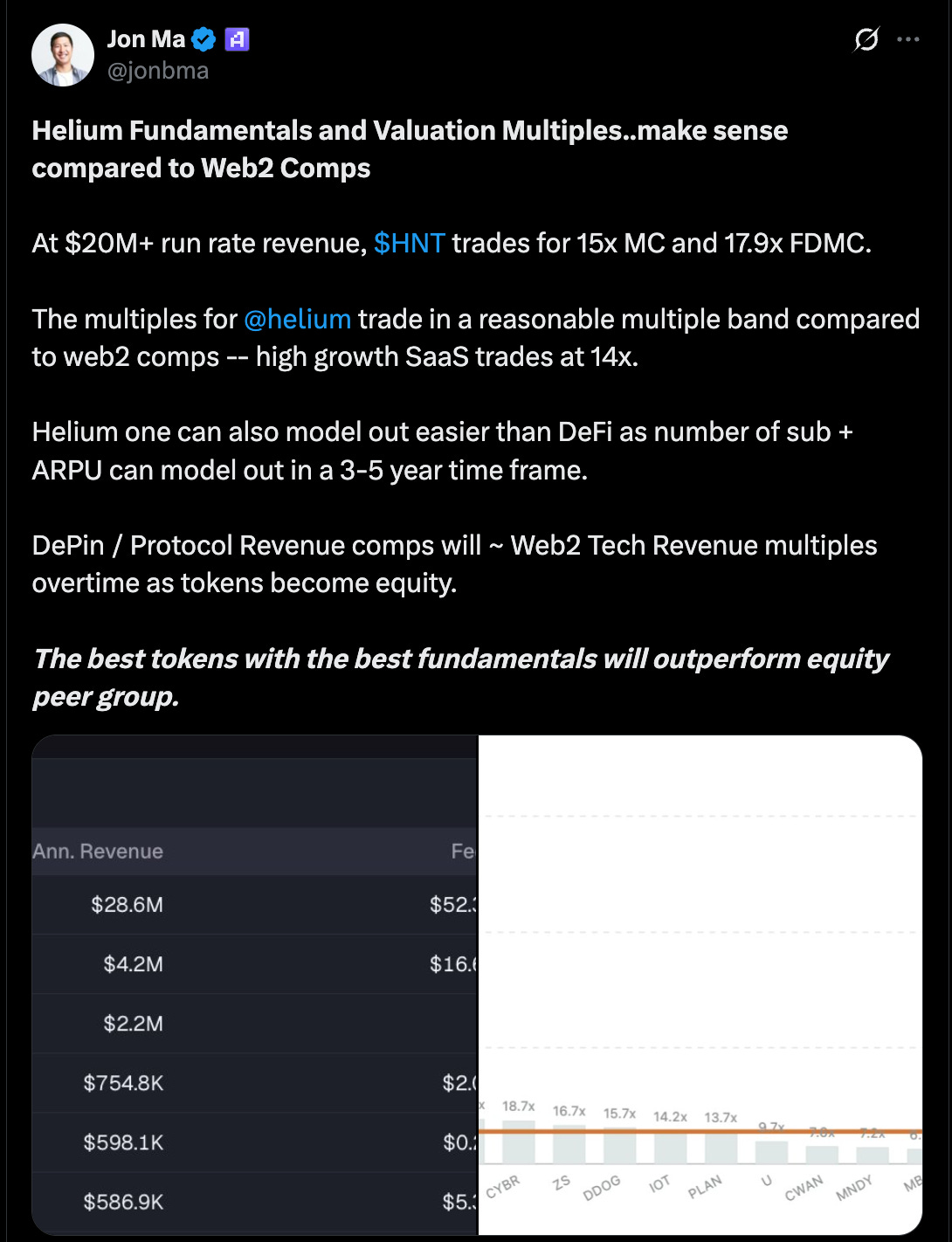

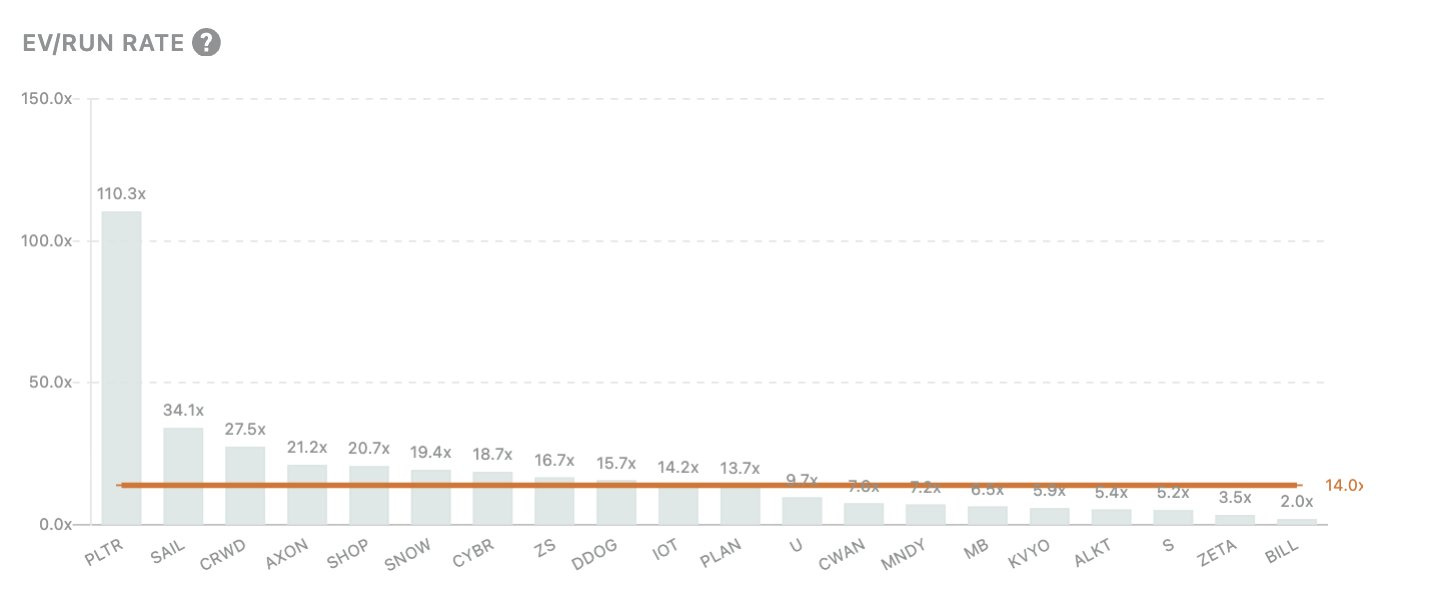

Helium, a DePin protocol that allows the supply side to deploy hotspots and get paid for sharing their internet and the demand side to pay for free to cheap mobile plan, is ~$20m run rate revenue and trades for 15x (MC) and 17.9x (FDMC).

High Growth SaaS businesses (granted at a much larger scale) trade at 14x revenue run rate (with the exception of Palantir)

We’re more or less seeing DeFi / DePin and applications trade on revenue multiples whereas for blockchains its less clear.

2. How do we value Base and Blockchains?

That’s why I was so excited when the JPM North America research team put out a piece valuing Base, an Ethereum Layer 2, at $12-$34B marketcap opportunity in their recent piece and accruing $4b-$12B to Coinbase equity — raising their price target to $404 (+12% at today’s prices) at end of the year Dec ‘26.

How should we value blockchains?

That’s been the challenge I’ve had since looking into L1s when I was an analyst at Whale Rock (L/S Fund).

At first we went through the developer activity and Daily Active Address meta but now with more and more applications that are building on top of these blockchains, there are conceivable ways to aggregate economic activity like Total Economic Activity which our team proposed: https://www.artemisanalytics.com/resources/reading-the-tea-total-economic-activity-leaves-the-metric-that-matters-for-blockchains

JPM valuing Base in a sell-side report felt like a watershed moment for Wall Street finally embracing onchain businesses and guiding the industry into a better way of valuation blockchains.

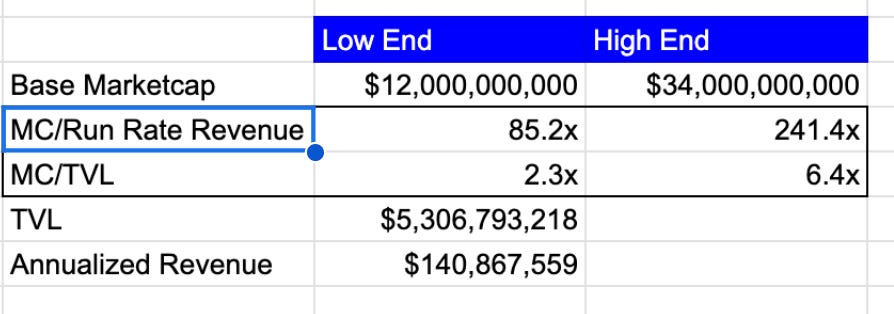

Let’s go through the numbers for how JPM justified a $12-$34B marketcap for Base.

Base is an Ethereum Layer2 built on the OP Stack and is exploring launching a token.

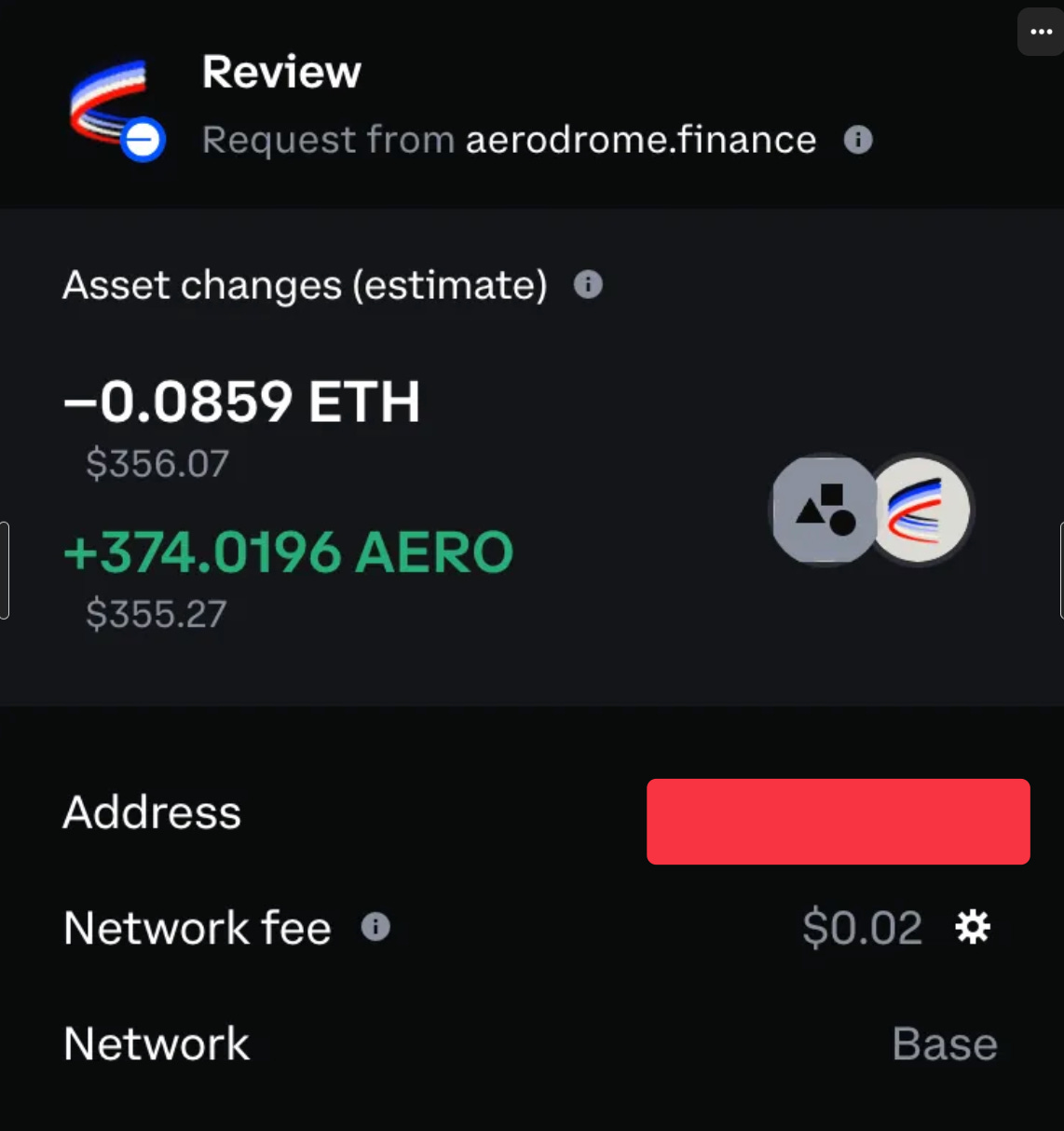

As an Ethereum Layer2, Base gets transaction fees when users pay to, say, swap on Aerodrome (leading Base decentralized exchange) one token for another token. In this swap, the user would need to pay $0.02 for the transaction.

As an ETH L2 built on OP Stack, Base needs to pay a subset of the fees to Ethereum for Data and Settlement, and Optimism Collective.

The remaining fees or what Artemis defines as revenue goes to the Coinbase sequencer which Coinbase can keep for the equity business..

The gap between user fees (L1 + L2 fees) and revenue is quite tiny.

Here are Base’s KPIs:

- Daily Active Users are 870k down from the near peak of ~2.4M in May ‘25.

- Base Transactions continues to trend upwards hitting nearly 80M / day

- TVL (or I like to think of as AUM on a chain) is basically at all time at ~$5B

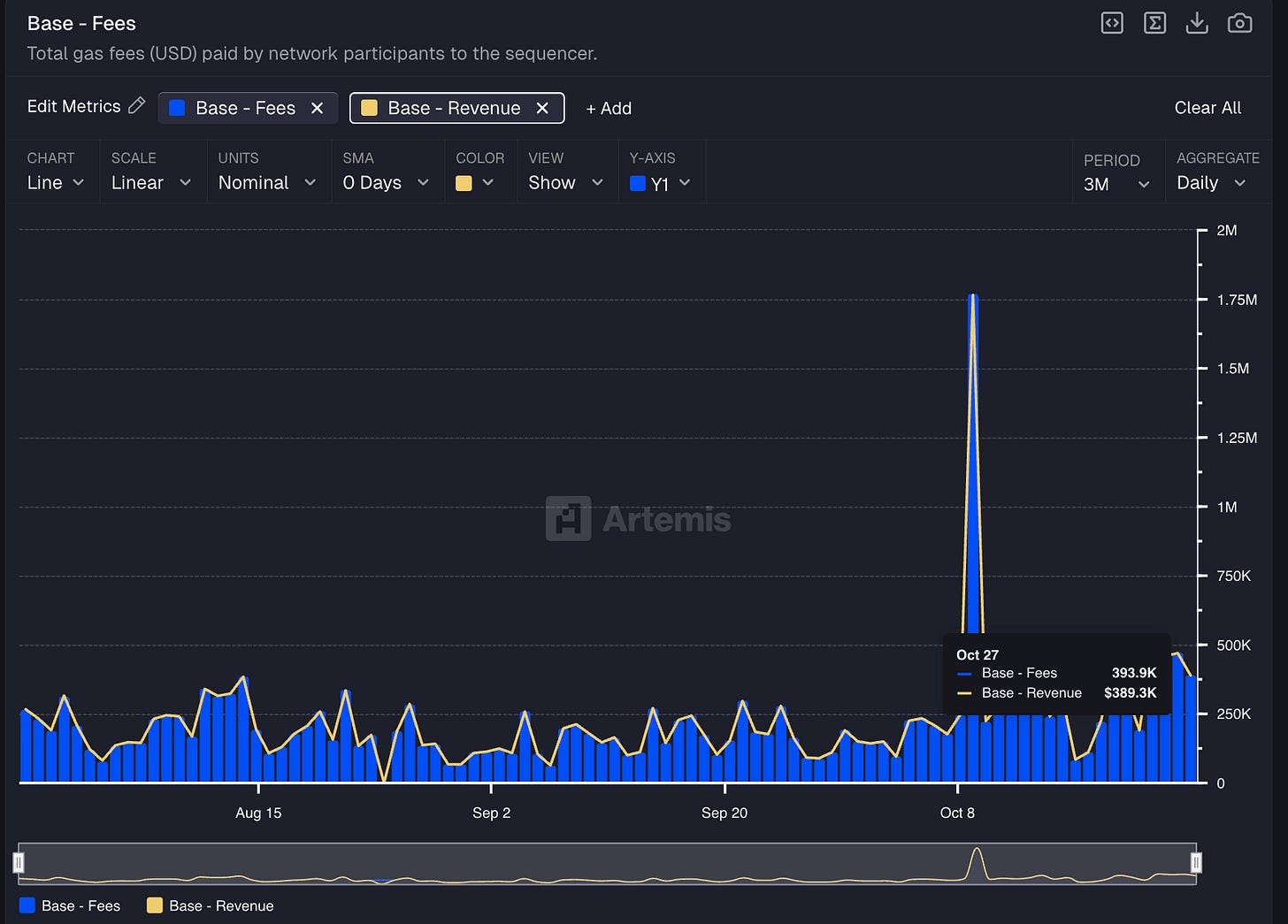

- Fees paid by users continue to cycle up and down — ~$135M annualized fees if you take the last week and multiple by 52.

Base is a dominant chain if you zoom out as the #4 chain by Daily Active Users, #3 by chain transactions, #4 in TVL and #5 by revenue.

The JPM sell side research team targets Base as $12-$34B in marketcap.

From our metrics, that puts Base at anywhere between 85.2x-241.4x revenue run rate (Fees)

Blockchains are notoriously hard to value because the revenue multiples on a circulating market cap range from 10.9x for Hyperliquid to 1,160x for NEAR

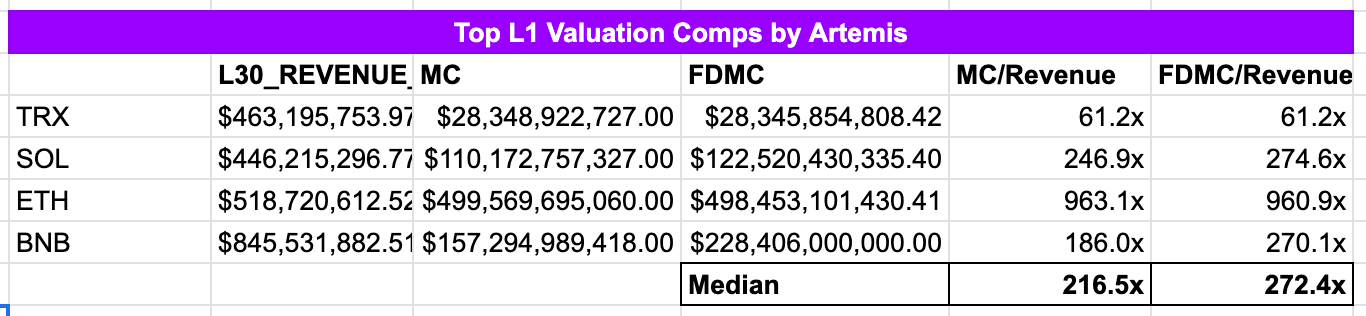

If we use Binance, Ethereum, Solana, Tron as the peer set for Base, the 241.4x Base revenue run rate..isn’t crazy.

The Median MC/Revenue is 216.5x and FDMC/Revenue is 272.4x.

The question then is, what are the steady state revenue multiples for these blockchains and is revenue even the right metric for these networks to optimize for?

Tempo, the payments blockchain, recently raised $500m at $5B. What if Tempo takes on majority of stablecoin payment volume but takes very little fees — should the network be valued less for charging merchants and customers less even though there are larger amounts of payment volume that flow through the network?

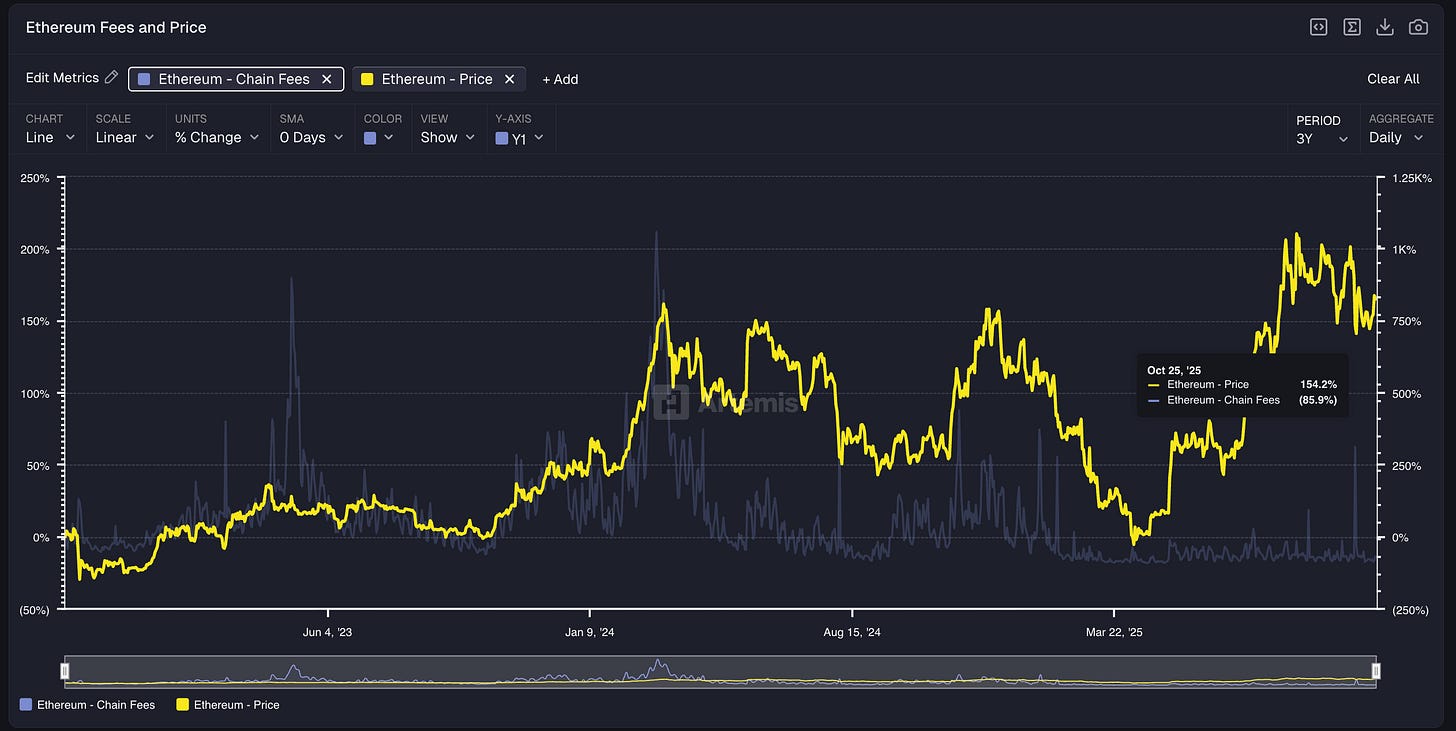

Is it objectively worse for Ethereum for lowering gas fees through the various Ethereum Improvement Proposals if there is more overall activity and settlement on ETH?

Clearly it doesn’t matter to markets as Chain fees for Ethereum are down 82% in the last 3 years but ETH price is up 167%

This is a question Wall Street, Buy Side / Sell Side and the foundations need to figure out: what is the metric that matters for blockchains and what blockchains are optimized for and that chains, sell side and buy side should guide towards.

3. Stablecoins Update

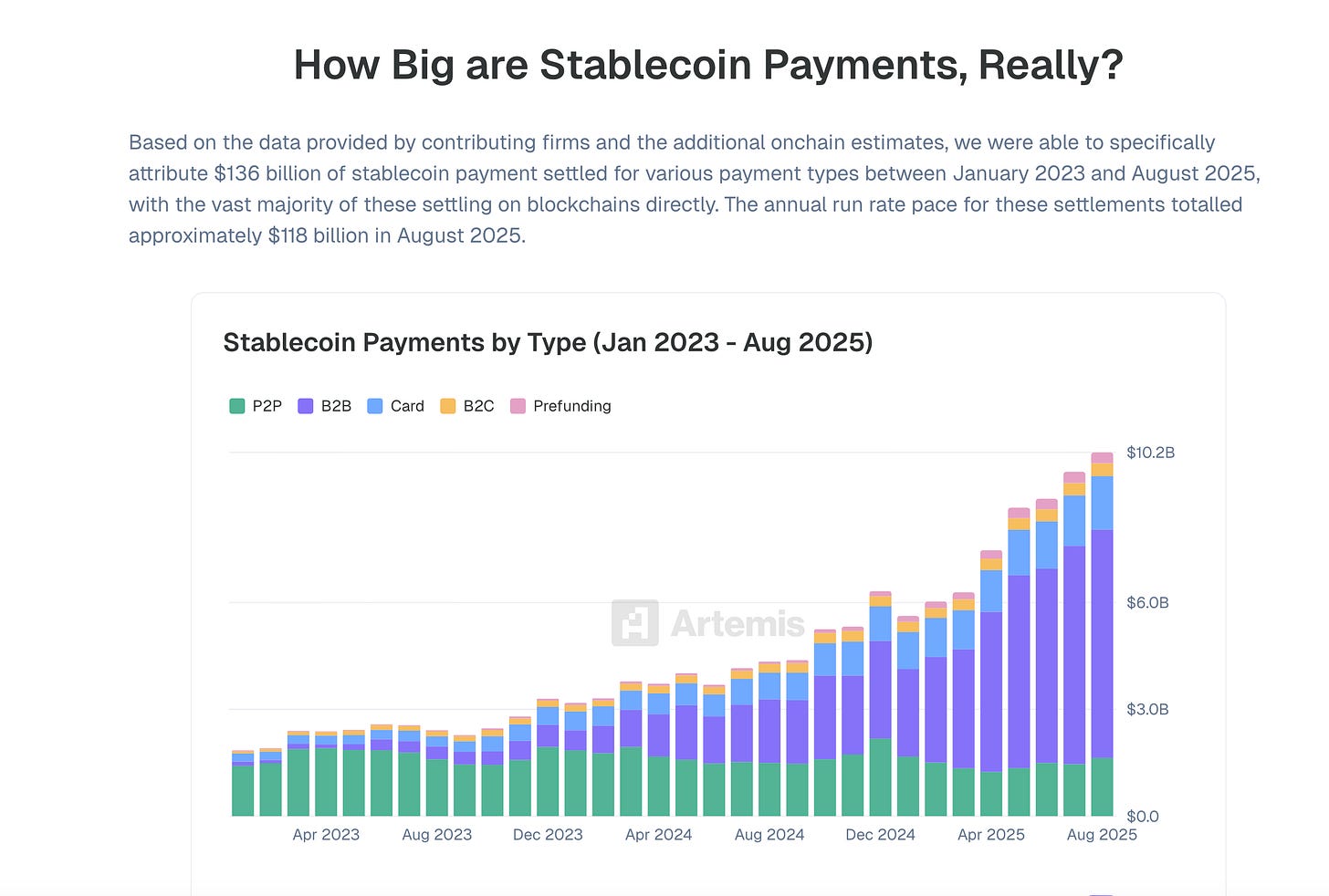

We launched Part 2 of our stablecoin report with Castle Island Ventures and Dragonfly by working with 30+ partners to get proprietary stablecoin data to answer the golden question: how much of stablecoin volume onchain is real.

Let’s be honest, the chart of total stablecoin transfer volume isn’t particularly useful even though its large ($6.1T per month or ~$72T annualized)

We can cite $6T of onchain stablecoin transfer volume but a large amount of the volume can be centralized exchange hot wallets transfering large amount of stablecoin volume, DeFi protocols swapping large amounts of stablecoins for their onchain DEX design, or MEV or bots transfering large amount of stablecoins that aren’t indicative of organic activity.

That’s why the correct way to calculate ACTUAL REAL stablecoin payment volume is to work directly with the leading stablecoin payment players to create a view bottoms up how much volume is there.

We finally got our answer for August 2025: $122B of run rate up 137% YoY or ~0.17% of all stablecoin transfer volume is used for payments.

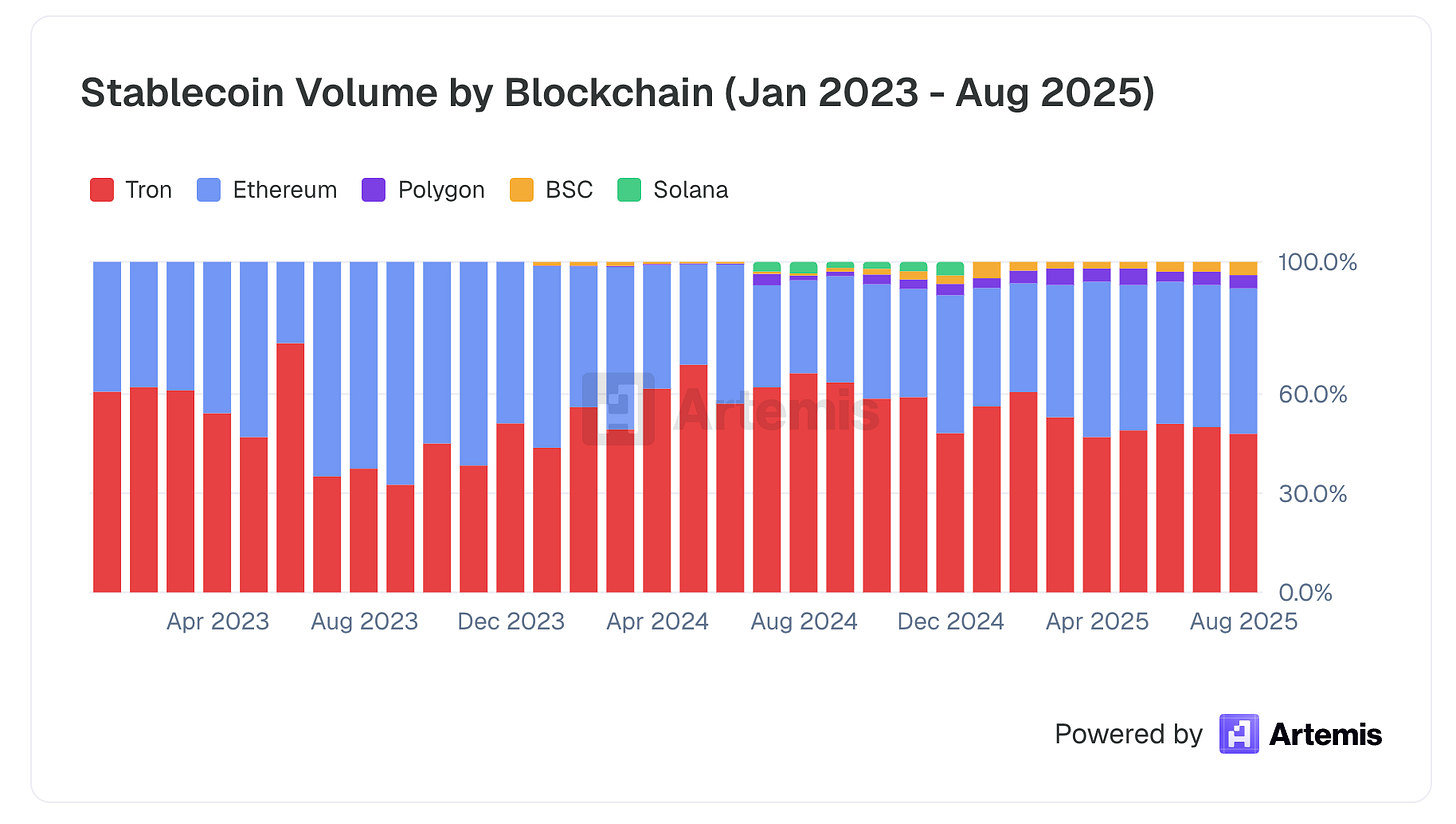

I found it particularly interesting to see that Polygon and Binance growing its share of real payment volume as the Ethereum / Tron monopoly is shifting to other blockchains.

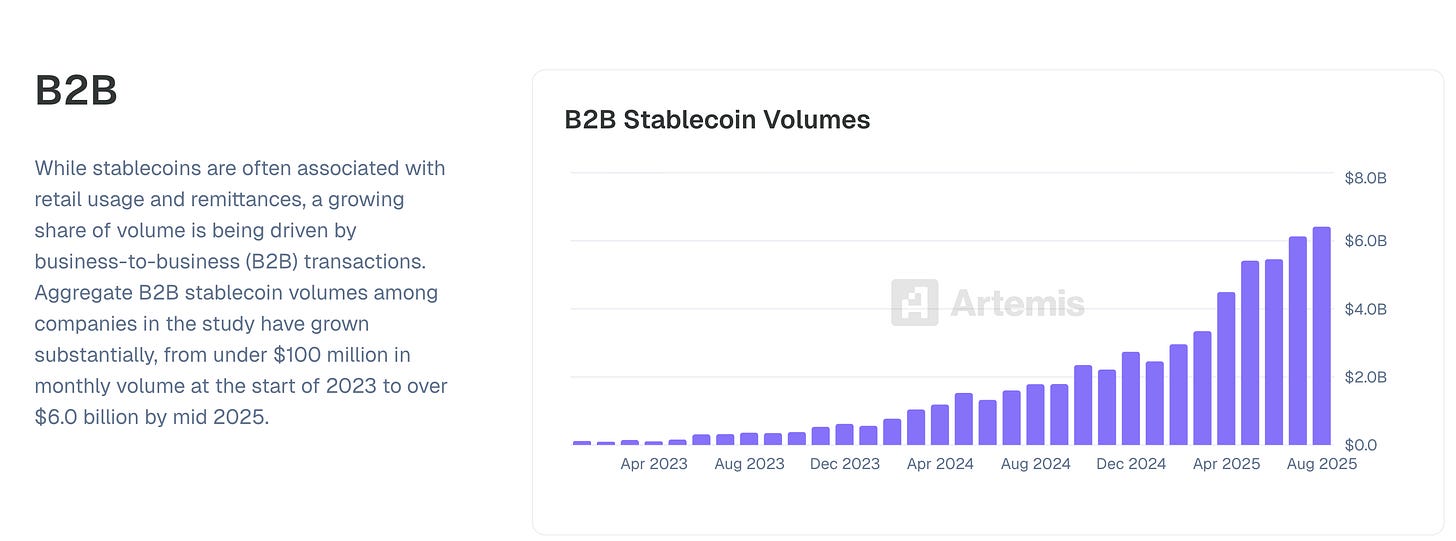

In addition, B2B Stablecoin Volumes is up $76.8B run rate up 255% YoY — these are the types of transactions a PSP would enable and we define B2B transactions as business making a payment for goods or services to another business.

As always, if you are interested in our valuation templates for Base, comp tables for L1s or want to chat about stablecoins, feel free to leave a comment below or ping us at team at artemis dot xyz.

Cheers,

Jon